The Research

Everything we have published, organised by date. We are personal finance researchers, not advisors. Every article on this site is plain-English education, never prescription. Browse by topic above the grid, or scroll through the latest research below.

141 articles

What a payday loan is, how it works, and what it really costs: the 391% APR, the rollover debt cycle, payday vs personal loans, and how India's instant-loan-app reality compares.

14 min read

What a joint bank account is and how it works, compared for the US and India: types and operating modes, deposit insurance (FDIC vs DICGC), survivorship, and the risks.

13 min read

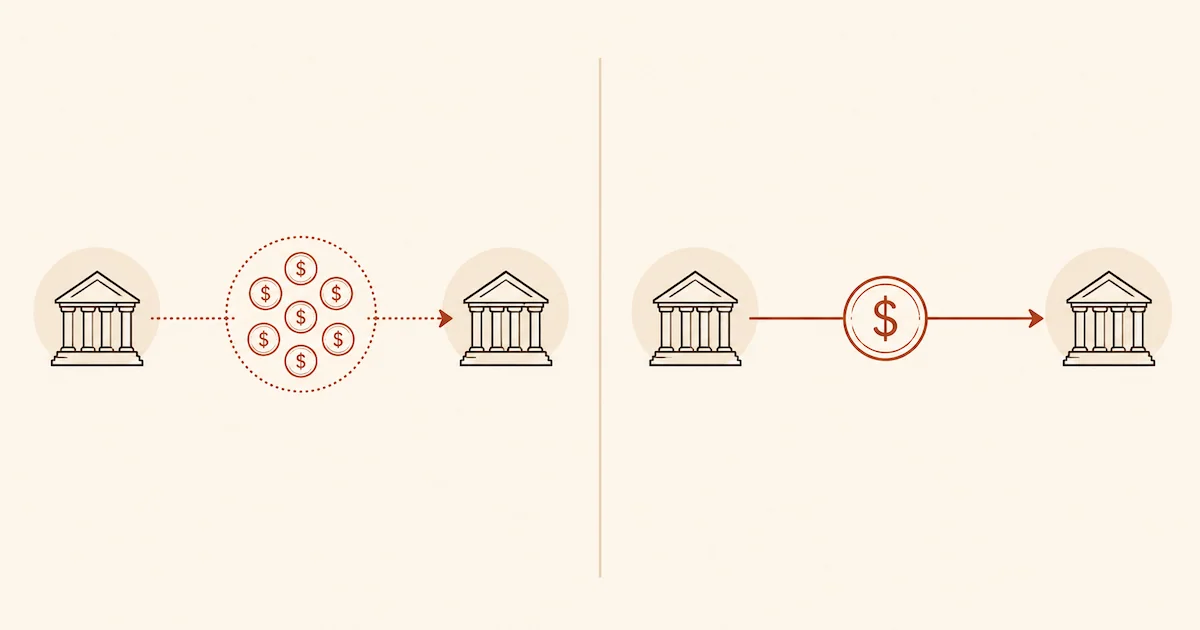

Wire transfer vs ACH compared on speed, cost, reversibility, and safety, with a full table, where FedNow and RTP fit, and how it maps to India's NEFT, RTGS, and UPI.

12 min read

Saving money isn't 50 random tips, it's a short ordered system. The hierarchy that actually moves the number, with worked ₹ and $ examples, for India and the US.

12 min read

A biweekly budget plans each two-week paycheck on its own. Budget on two checks a month as your floor, and the year's two extra paychecks become surplus.

13 min read

A debit card spends your money; a credit card borrows and bills you later. The real differences in fraud liability, disputes, credit-building, fees, and interest.

12 min read

Dropshipping is selling products you don't stock, with the supplier shipping direct. A neutral explainer: how it works, the real net margins (not the gross), why most stores fail, and how it differs in India and the US.

12 min read

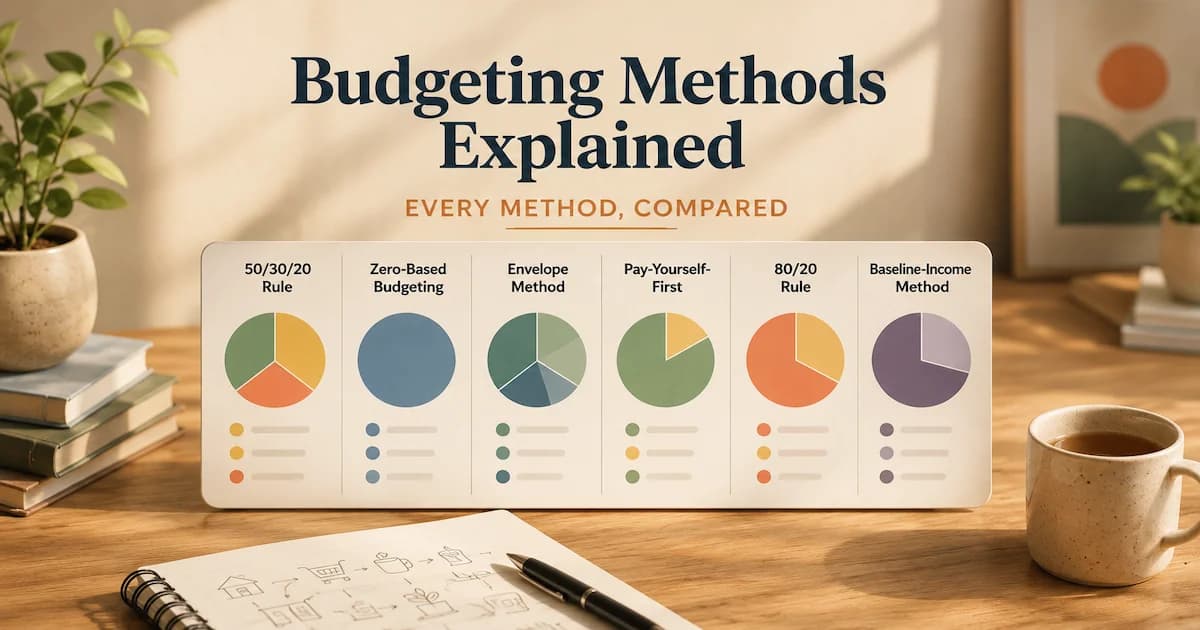

Every personal budgeting method compared side by side, with worked examples in ₹ and $, a guide to which method fits you, and an honest note on where each one fails.

13 min read

A recession is a significant, broad-based decline in economic activity that lasts more than a few months, visible across GDP, jobs, income, and spending. How the two-quarters rule of thumb differs from the official NBER definition, how recessions are dated, and what happens in one.

9 min read

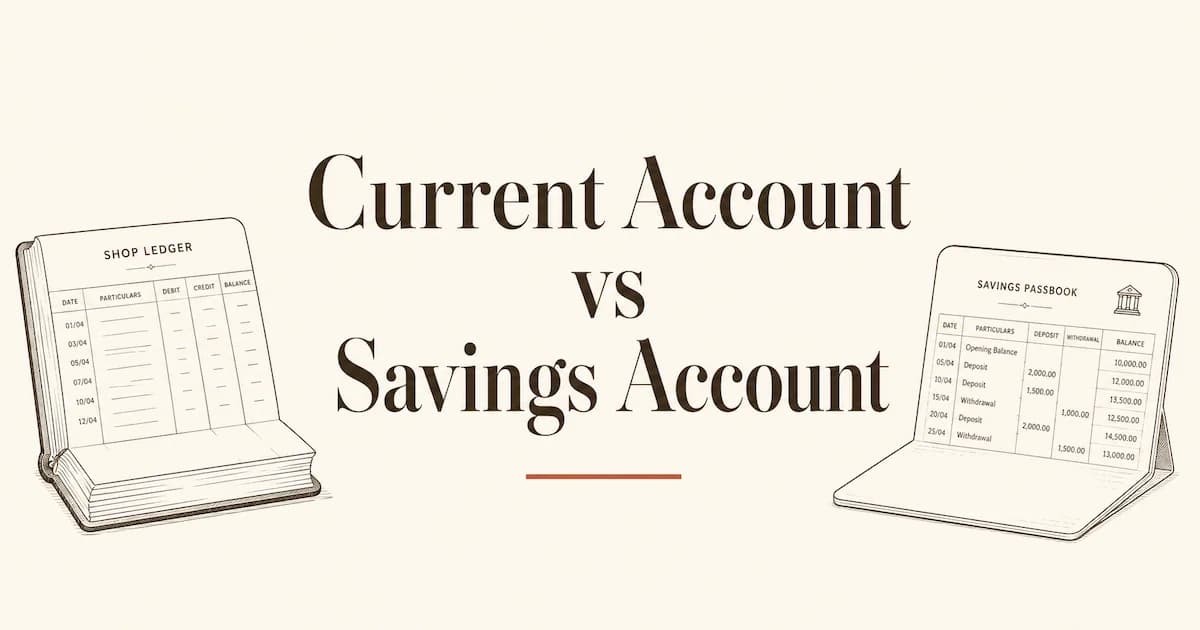

Current account vs savings account in India: a current account is a non-interest bank account built for businesses and high-volume transactions, while a savings account is an interest-bearing account for individuals. How they differ on interest, transaction limits, and minimum balance.

9 min read

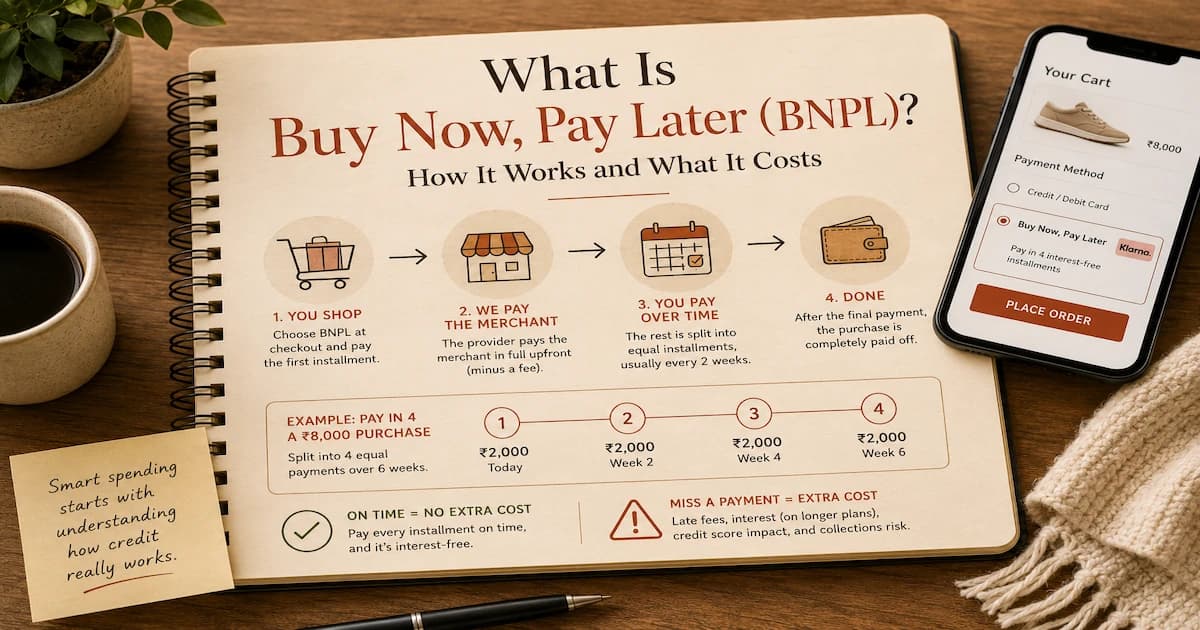

Buy Now, Pay Later (BNPL) splits a purchase into a few interest-free installments. How the 'pay in 4' model works, what it really costs, and how it compares to a credit card.

9 min read

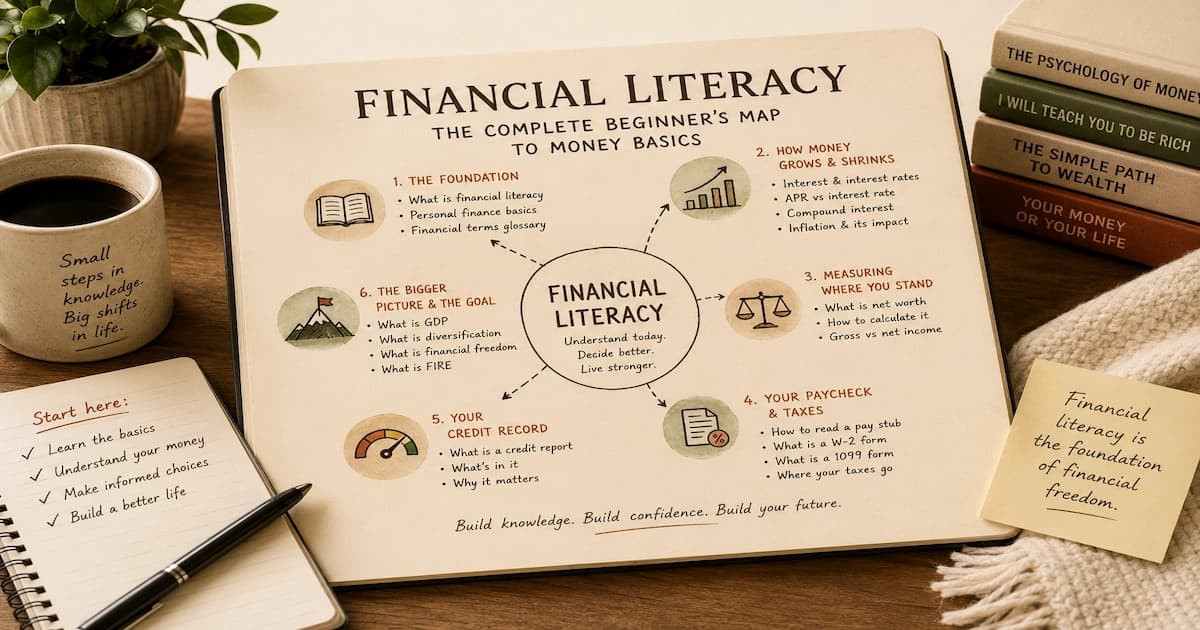

Financial literacy is understanding core money concepts well enough to make informed decisions. This pillar maps the basics, interest, inflation, net worth, pay stubs, credit, taxes, in plain English.

13 min read

Gross Domestic Product (GDP) is the total value of goods and services a country produces. What it includes, its four components, real vs nominal, and what it misses.

9 min read

How to check your CIBIL score for free in India, what the 300-900 score means, the four RBI-licensed bureaus, the one-free-report-a-year rule, and the steps.

9 min read

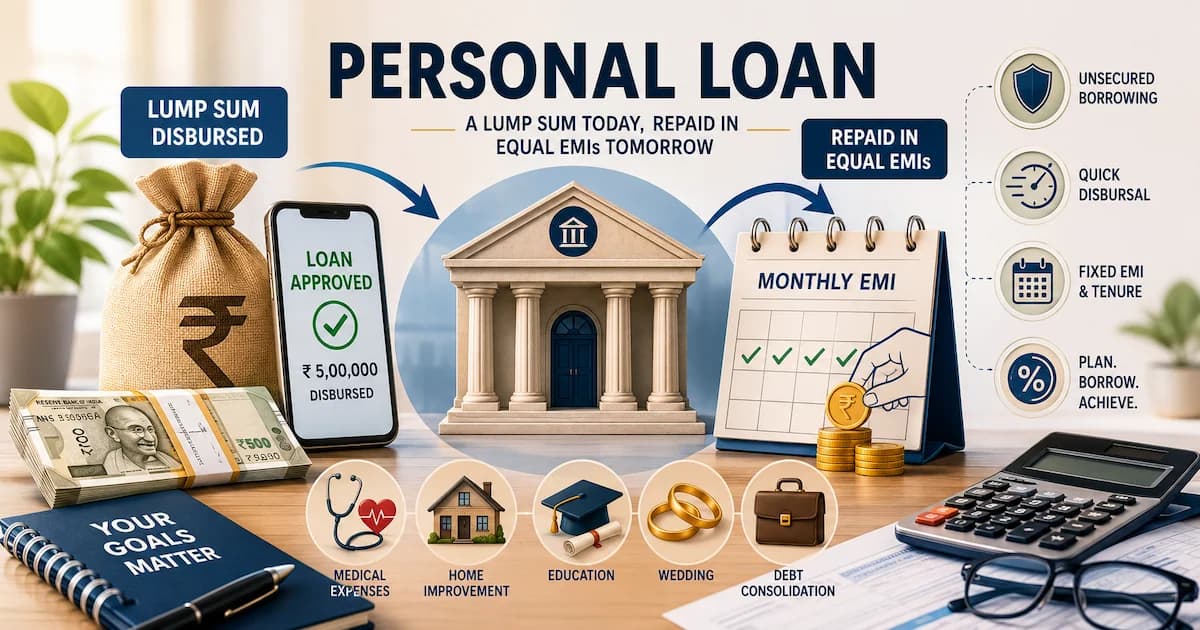

A personal loan is an unsecured installment loan repaid in fixed EMIs. How it works, secured vs unsecured, the real cost, and how it compares to a credit card.

9 min read

A pillar guide to India's government savings schemes, PPF, EPF, NPS, SSY, APY, SCSS, POMIS, NSC, KVP, SGB and PMJJBY/PMSBY, with current Q1 2026 rates, tax treatment, and where each fits.

12 min read

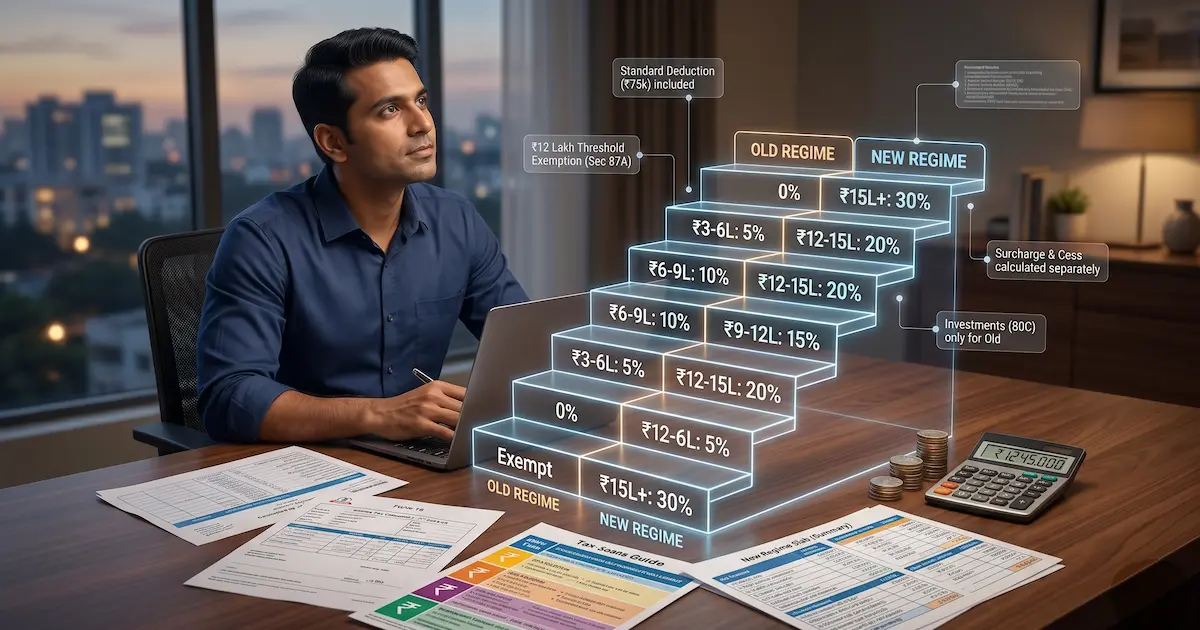

Complete India income tax guide for salaried employees for FY 2025-26 (AY 2026-27), new vs old regime, Form 16, HRA, 80C, capital gains, ITR-1 vs ITR-2, step-by-step filing, common mistakes, and when to consult a CA.

26 min read

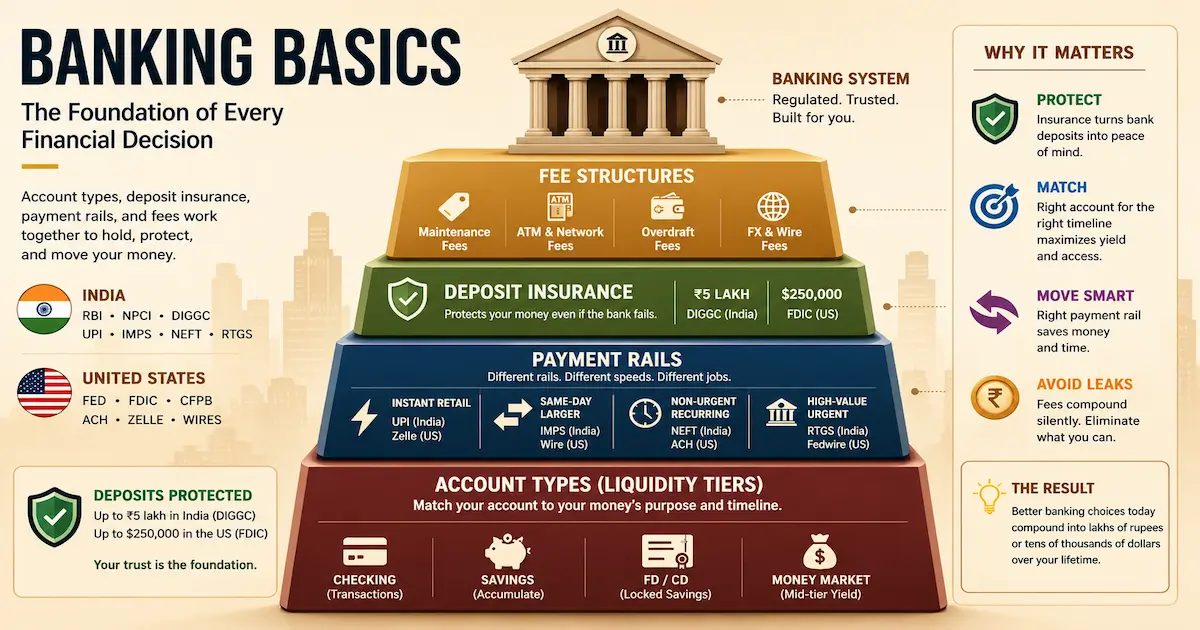

What is banking? A comprehensive introduction to the account types, payment rails, deposit insurance, and fee structures that form the foundation of personal finance. Covers checking and savings accounts, fixed deposits and CDs, FDIC and DICGC deposit insurance, UPI and the India payments stack, US ACH and wire transfers, overdraft protection, money market accounts, and bank fees, for India and US audiences.

11 min read

Herd mentality in investing is copying the crowd instead of your own analysis. How it works, the India and US bubbles, what it costs, and how to spot it.

13 min read

What is hyperbolic discounting vs the endowment effect? Two advanced behavioural-finance biases, hyperbolic discounting (the asymmetric preference for immediate rewards over delayed ones) and the endowment effect (overvaluing things you already own). Covers Laibson's 1997 hyperbolic discounting research, the Kahneman-Knetsch-Thaler 1990 mug experiment, the retirement-saving problem, the future-self continuity research, and the structural mitigations that work for each.

10 min read

Behavioral finance is how psychology bends money decisions. See the biases table (cognitive vs emotional), what each one costs, and how to counter it.

13 min read

FOMO in trading is buying because others are profiting. The warning signs, real examples (GameStop, crypto, hyped IPOs, India F&O), and how to avoid FOMO trades.

14 min read

Mental accounting is why a bonus feels different from salary, though every rupee spends the same. Real examples, the investing trap, and how to beat it.

12 min read

What is GST in India? The Goods and Services Tax, a comprehensive destination-based indirect tax introduced on 1 July 2017 that subsumed 17 earlier central and state-level taxes. Covers the 5-slab rate structure (0%, 5%, 12%, 18%, 28% + cess), the CGST/SGST/IGST split between centre and state, Input Tax Credit, the GST Council, registration thresholds (₹40L for goods, ₹20L for services in most states), and the composition scheme for small businesses. For your specific business or filing situation, consult a Chartered Accountant or GST practitioner.

9 min read

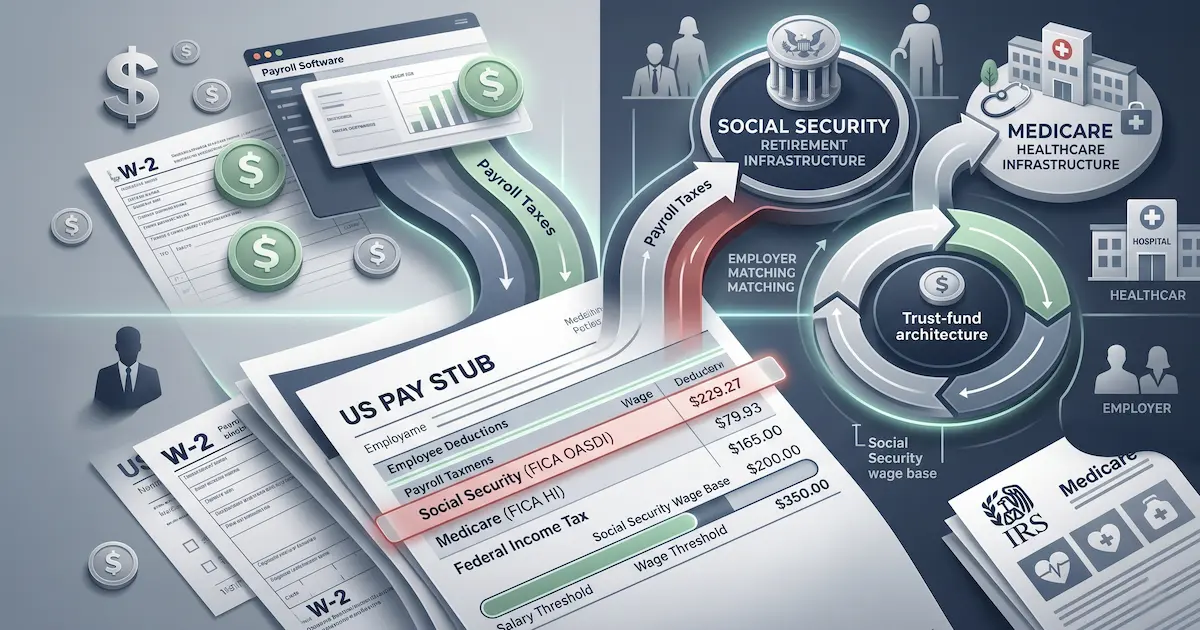

What is FICA tax in the US? The Federal Insurance Contributions Act payroll tax funding Social Security (6.2% on wages up to the wage base) and Medicare (1.45% on all wages, plus 0.9% Additional Medicare above income thresholds). Covers the 2025 wage base of $176,100, employer match doubling the total burden to 15.3% up to the wage base, self-employed treatment under SECA (Schedule SE), and brief comparison to India's EPF + ESIC payroll-based social security.

9 min read

Anchoring bias is leaning too hard on the first number you see. Classic experiments, real ₹ and $ examples in pricing, salary and investing, and how to reduce it.

15 min read

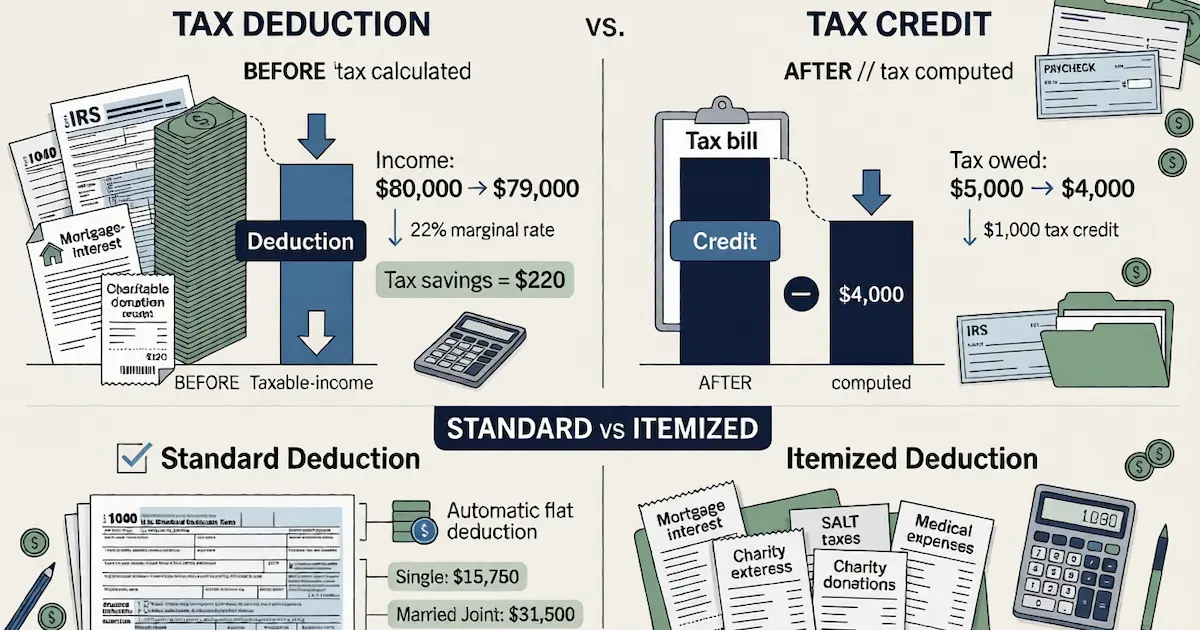

What is the difference between a tax deduction and a tax credit, and between standard and itemized deduction? Tax deductions reduce taxable income (worth your marginal rate × deduction amount); tax credits reduce tax owed dollar-for-dollar. Standard deduction is the flat IRS-fixed amount ($15,750 single / $31,500 married joint for TY 2025); itemized deduction sums specific expenses (SALT cap $10K, mortgage interest, charitable contributions, medical above 7.5% AGI). Covers the math, the structural distinction, and when each makes sense, for educational understanding, not filing advice.

10 min read

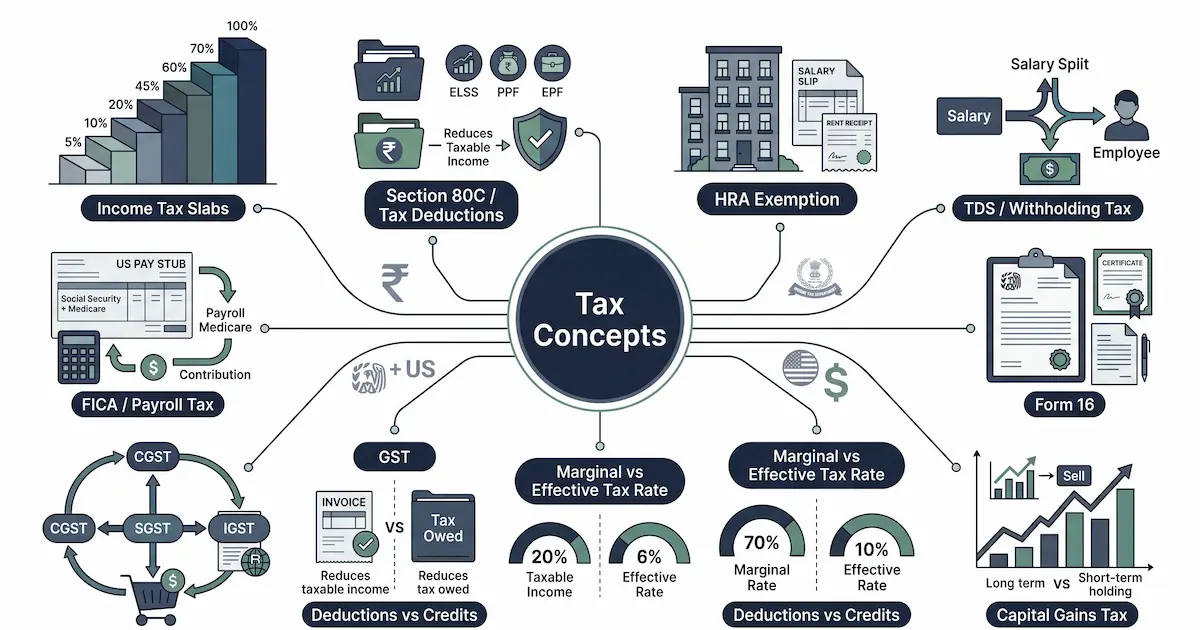

What are the foundational tax concepts every Indian and US taxpayer should understand? This pillar page synthesizes 10 definitional explainers covering income tax slabs (India new + old regime), Section 80C, HRA exemption, TDS, Form 16, capital gains, marginal vs effective tax rates, deductions vs credits, standard vs itemized deduction, GST, and FICA. Research-led definitions, not tax planning advice. For your specific situation, consult a Chartered Accountant (India) or Certified Public Accountant (US).

12 min read

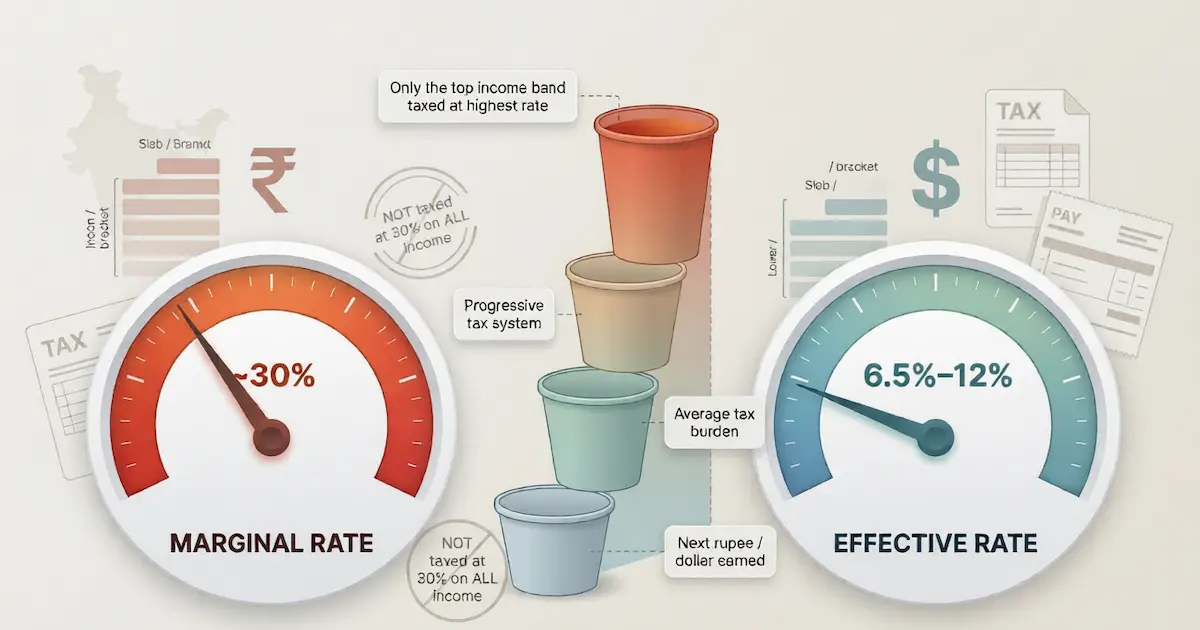

What is the marginal tax rate vs the effective tax rate? Two related but distinct concepts in progressive tax systems. Marginal rate is the percentage applied to your next rupee or dollar of income; effective rate is total tax divided by total income. Covers worked examples for India (new regime ₹15L salary at 15% marginal / 6.5% effective) and the US (federal marginal 22% / effective ~12-14% typical), the most common bracket misconception, and why each rate matters for different decisions.

9 min read

A sunk cost is what you already spent and cannot recover; the sunk cost fallacy is continuing only because of it. Examples from the Concorde to a losing stock, and how to avoid it.

13 min read

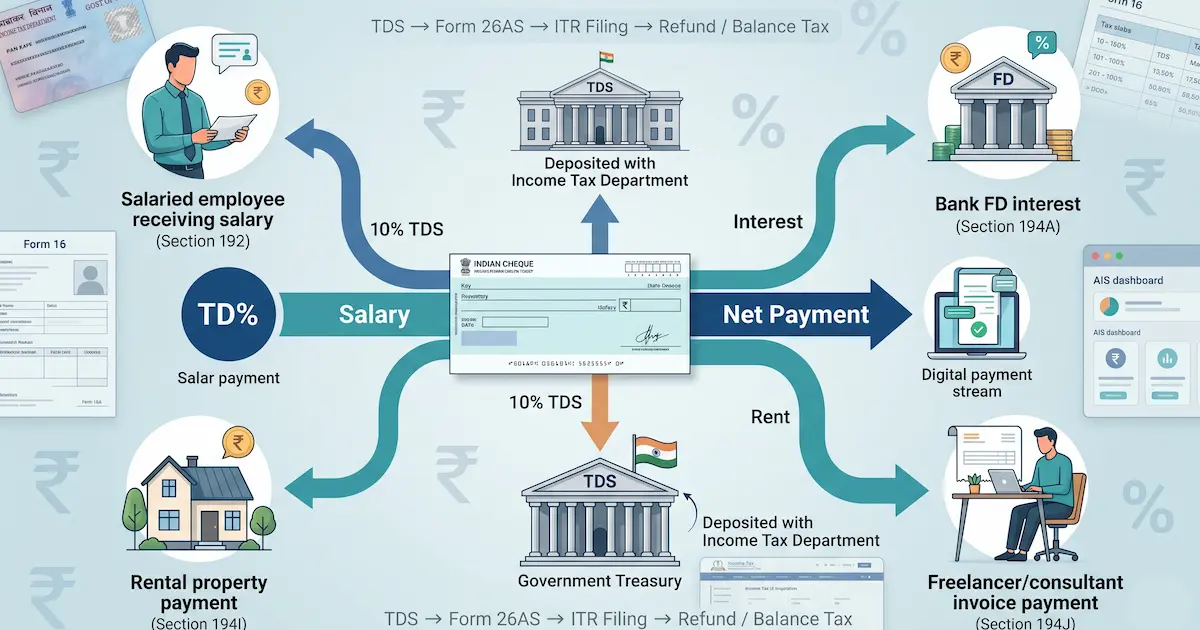

What is TDS? Tax Deducted at Source, the mechanism where the payer of certain income deducts tax before paying the recipient and deposits it with the government. Covers Section 192 (salary), 194A (interest), 194I (rent), 194J (professional fees), 194C (contractor payments), 194 (dividends), the PAN requirement under Section 206AA, current FY 2025-26 thresholds, and how TDS reconciles against ITR liability via Form 26AS.

9 min read

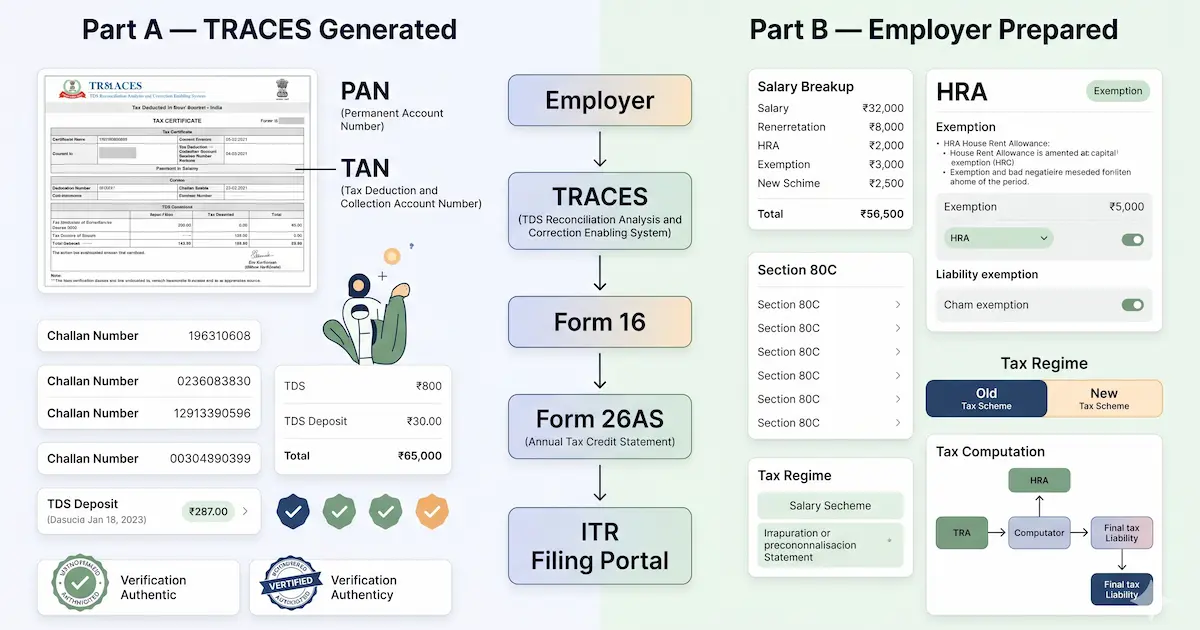

What is Form 16? The TDS certificate Indian employers issue to salaried employees under Section 203 of the Income Tax Act, documenting tax deducted from salary across the financial year. Covers Part A (TRACES-generated, TDS quarter-by-quarter) vs Part B (employer-prepared, salary and deduction breakup), the June 15 issuance deadline, Form 16A for non-salary TDS, how to reconcile Form 16 against Form 26AS, and what to do about mismatches.

9 min read

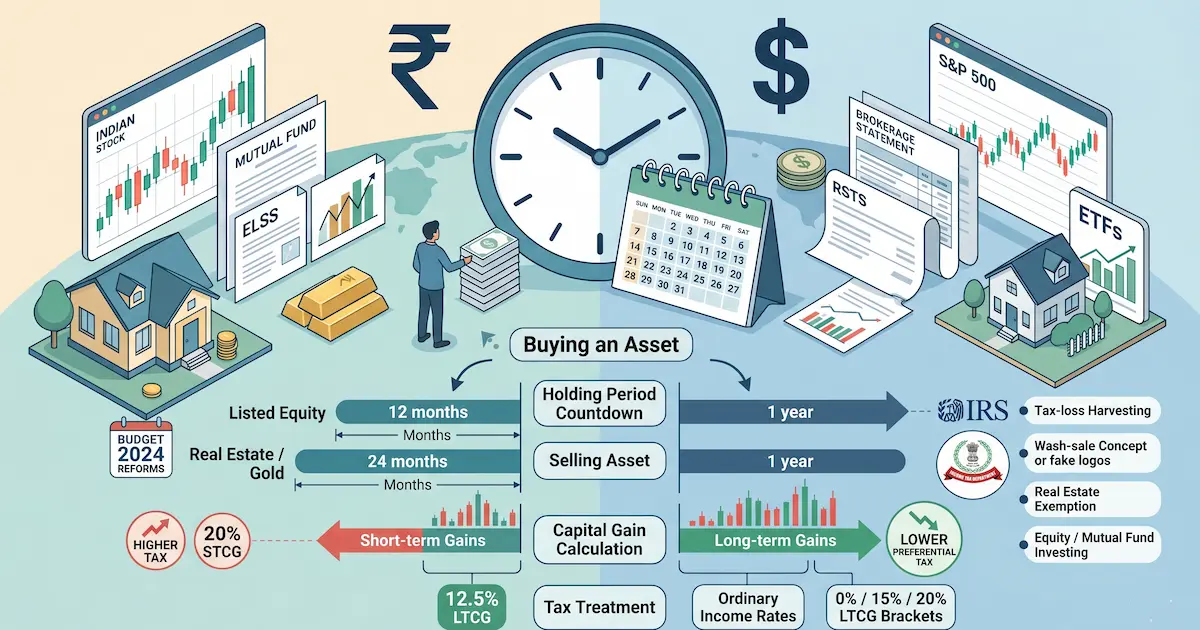

What is capital gains tax? The tax on profit from selling a capital asset, with rates depending on how long you held it. Covers India's post-Budget-2024 rates (12.5% LTCG on equity above ₹1.25L, 20% STCG on equity, 12.5% LTCG on all other assets without indexation, 12-month / 24-month holding periods) and the US structure (0/15/20% long-term rates by income, ordinary slab rates on short-term). Includes worked examples in both countries.

10 min read

What are the bank fees you're actually paying? Monthly maintenance, overdraft, ATM, wire, foreign transaction, minimum balance penalties, SMS alert charges, debit card annual fees, covers the full fee surface at both US and Indian banks, with current Q1 2026 fee schedules, the waiver conditions that eliminate most fees, and the structural choice of online vs traditional banks that determines the baseline.

10 min read

Lifestyle creep is spending that rises to match income; the latte factor is small daily spends compounding. The honest math, the critique, and ₹ and $ examples.

15 min read

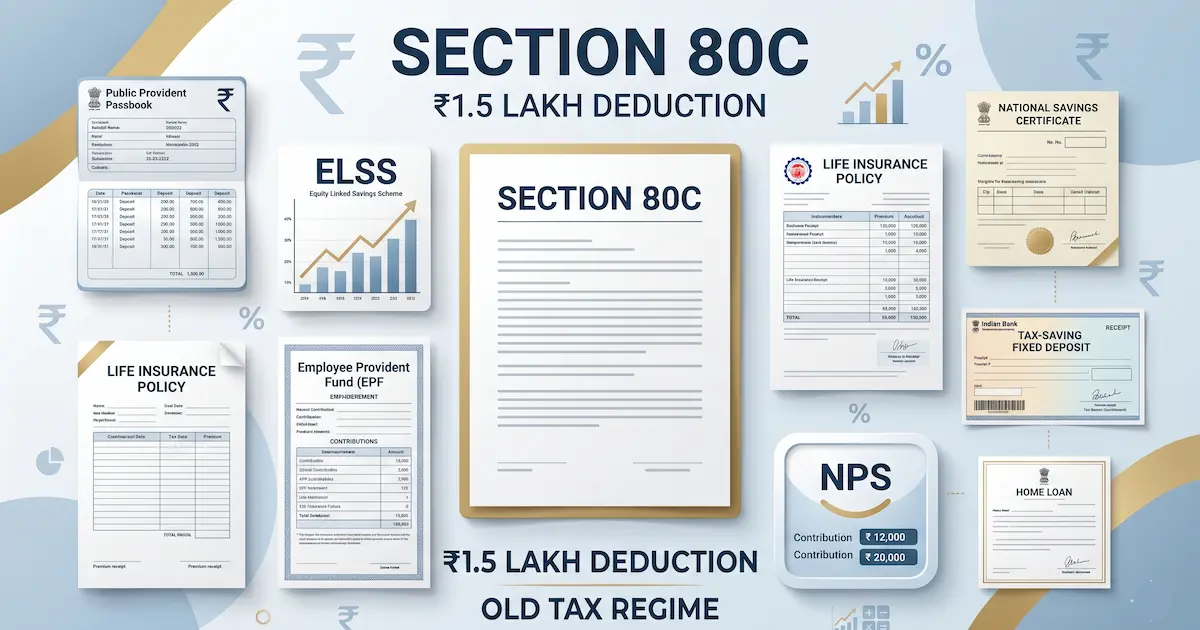

Section 80C cuts up to ₹1.5 lakh off taxable income for PPF, ELSS, LIC, EPF and more, but only under the old regime. The 2025-26 list, limit, and how to claim.

13 min read

What is overdraft protection? An opt-in bank service that covers transactions exceeding your account balance, usually for a $35 average fee per occurrence in the US (CFPB data). Covers how overdraft fees work, the Regulation E opt-out, the cheaper alternative of linking a savings account, and India's overdraft facility (OD against FD or salary) which functions differently from US overdraft protection.

9 min read

Loss aversion is feeling losses about twice as intensely as equal gains. The 2.25 ratio, examples, loss vs risk aversion, and how it quietly hurts returns.

14 min read

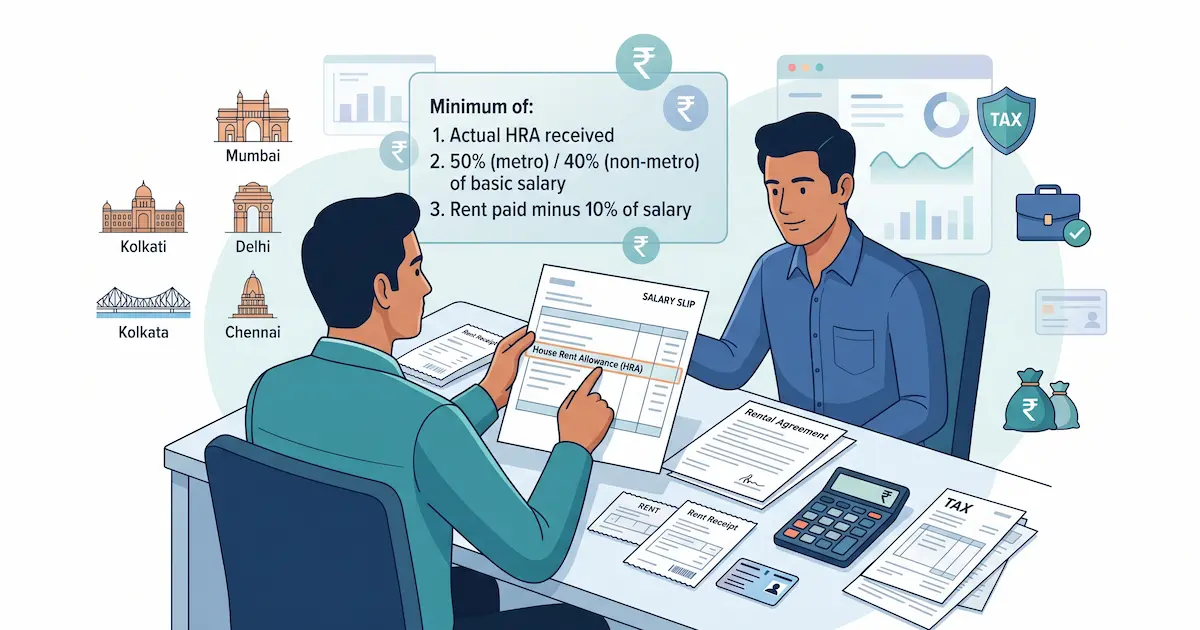

HRA exemption is the least of three amounts under Section 10(13A). See the FY 2025-26 formula, a worked example, metro cities, the limit, and the claim rules.

13 min read

What is a money market account (MMA)? A US deposit account that blends savings-account FDIC coverage with checking-account features, paying 4-5% APY at top online banks in Q1 2026, allowing limited cheque writing and debit card use, and requiring higher minimum balances ($1,000-25,000) than standard savings. Covers how MMAs differ from money market mutual funds, why India's liquid mutual funds fill the same role, and when an MMA beats a HYSA.

9 min read

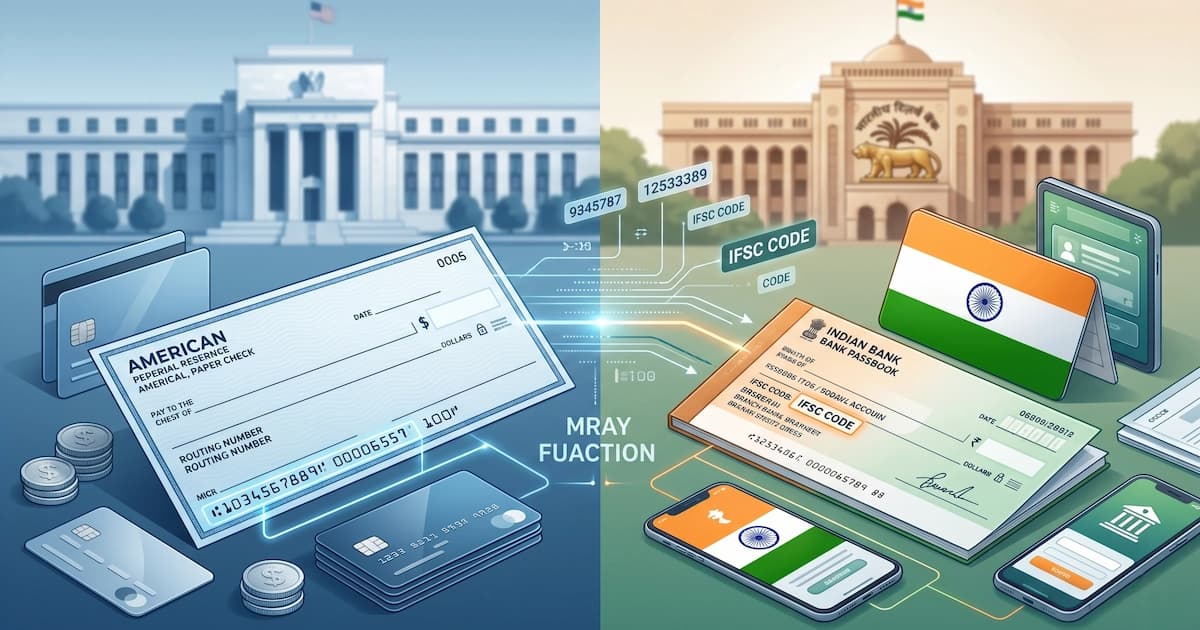

India uses IFSC codes; the US uses ABA routing numbers. See each format, the US-India equivalents, and the SWIFT code you need to wire money abroad.

13 min read

What is an income tax slab in India? The progressive-rate structure where different bands of income are taxed at increasing percentages. Covers the new regime slabs and old regime slabs as notified by the Income Tax Department for the current financial year, the Section 87A rebate that produces effective zero tax up to ₹12 lakh under the new regime, the standard deduction of ₹75,000, Health and Education Cess of 4%, and a fully worked example. For your specific situation, consult a Chartered Accountant.

10 min read

What is UPI? The Unified Payments Interface built by NPCI on RBI's mandate in 2016, instant 24/7 bank-to-bank transfers using a Virtual Payment Address (VPA). Covers the underlying architecture, transaction limits, the ₹16+ lakh crore processed monthly across 600+ member banks, autopay mandates, UPI Lite for small payments, and how the rails differ from IMPS/NEFT/RTGS.

10 min read

What is the difference between IMPS, NEFT, and RTGS? Three Reserve Bank of India payment systems with different speeds, limits, and use cases, IMPS is instant 24/7 up to ₹5 lakh, NEFT settles in 30-minute batches with no upper limit, RTGS is real-time for transfers ₹2 lakh and above. Covers fee structures, processing times, transaction limits, and which rail to pick for different scenarios.

10 min read

DICGC insures ₹5 lakh per Indian bank; FDIC insures $250,000 per US bank. The rules, what is and isn't covered, the 90-day payout, and FDIC vs NCUA vs SIPC.

16 min read

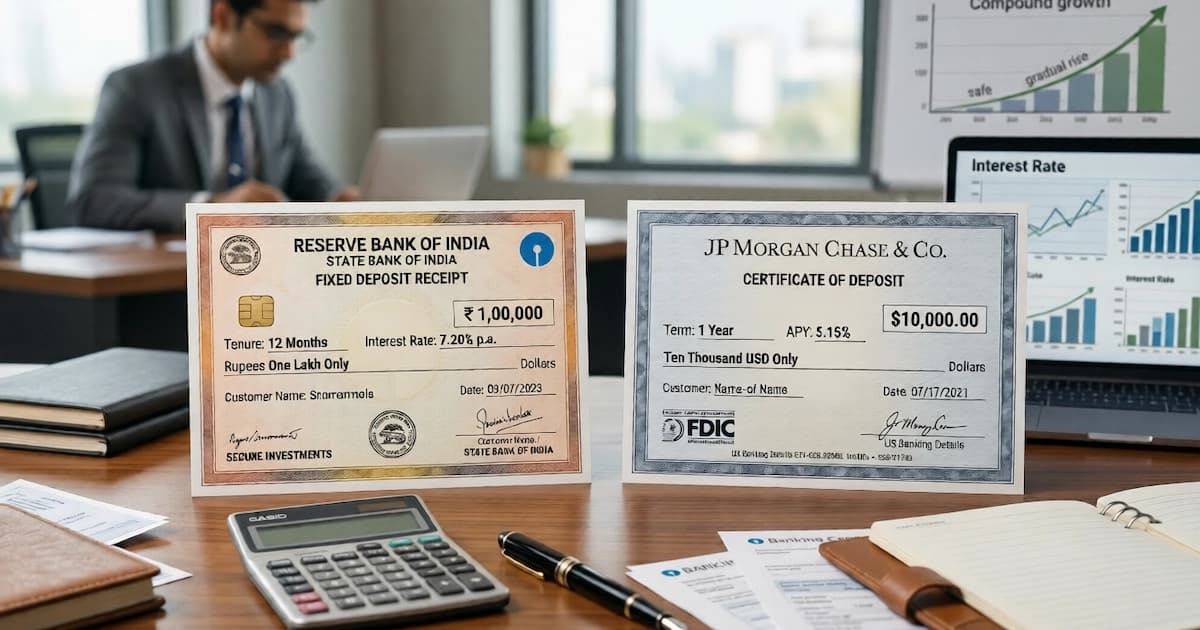

What is a fixed deposit (FD) in India and a certificate of deposit (CD) in the US? Both are time deposits, money locked at a fixed interest rate for a set tenure. Indian FDs paid 6.5-8% in Q1 2026 (small finance banks at the top end), US CDs paid 4.5-5.25% at online banks. Covers the math, the early-withdrawal penalty, DICGC vs FDIC coverage, and the senior-citizen rate bump.

10 min read

What is a savings account? An interest-bearing deposit account designed to park money you don't need immediately, paying 2.5-4% in Indian SB accounts, 0.46% in average US accounts, and 4-5% in US high-yield online savings. Covers how interest is calculated, the DICGC ₹5 lakh and FDIC $250,000 coverage limits, minimum balance rules, and the practical difference between savings and a fixed deposit.

9 min read

What is a checking account? A transactional bank account for daily spending, debit card, direct deposit, bill pay, paper checks, that typically earns 0.01-0.07% APY, charges $5-35 in monthly and overdraft fees, and sits under $250,000 FDIC coverage in the US. India has no direct retail equivalent: savings accounts handle the transactional role, current accounts are for businesses.

9 min read

What is Sukanya Samriddhi Yojana? The 8.2% interest rate, eligibility (girl child below 10), 15-year contribution + 21-year maturity, partial withdrawal at 18, and EEE tax treatment explained with worked example.

9 min read

What is Sovereign Gold Bond? The 2.5% annual coupon, 8-year tenure, gold-price-linked redemption, tax-free capital gains at maturity, and the 2024 discontinuation of new tranches explained.

9 min read

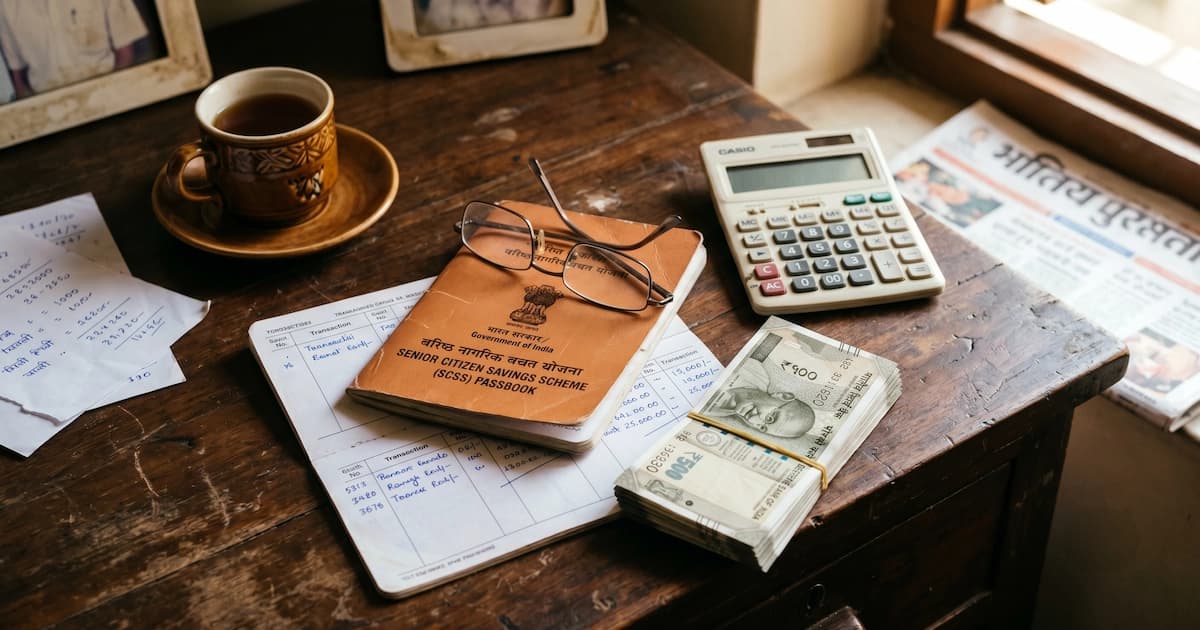

SCSS pays 8.2% for the Jul-Sep 2026 quarter, held since April 2023. The ₹30 lakh cap, quarterly payout, 5+3 year lock-in, 80C, and the new ₹1 lakh TDS rule.

13 min read

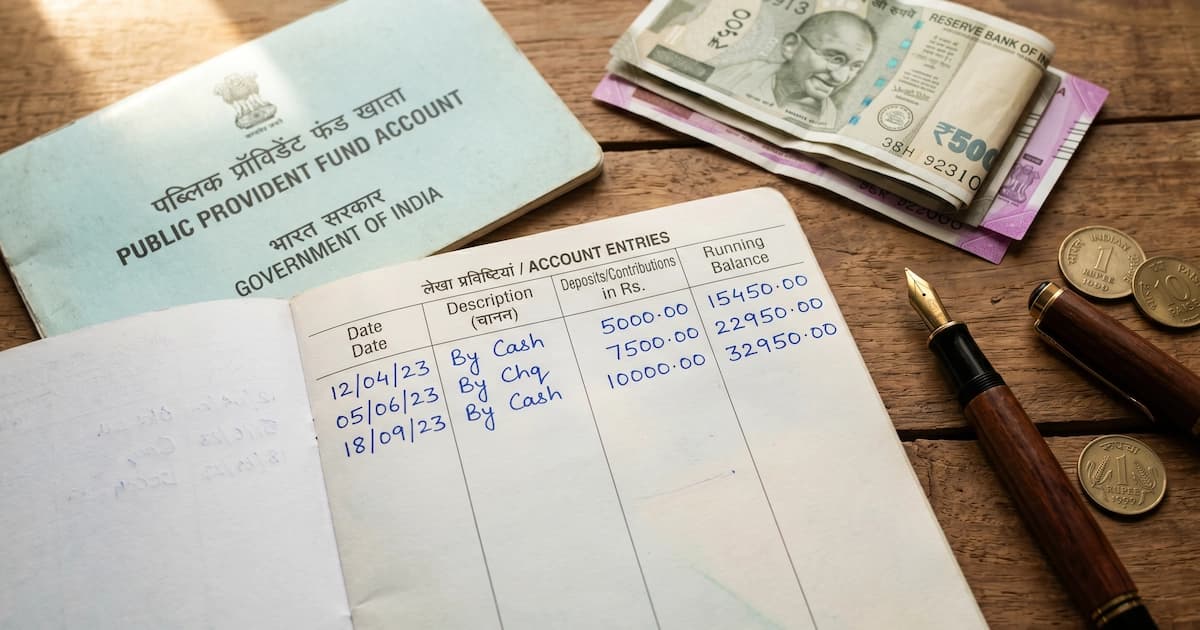

PPF pays 7.1% for Jul-Sep 2026, unchanged since 2020. See the Rs 500 to Rs 1.5 lakh limits, EEE tax, 15-year lock-in, withdrawal rules and a maturity example.

13 min read

Post Office Monthly Income Scheme (POMIS) pays 7.4% a year, credited monthly. A Rs 9 lakh deposit gives Rs 5,550 a month for 5 years. Payout table, limits and tax.

13 min read

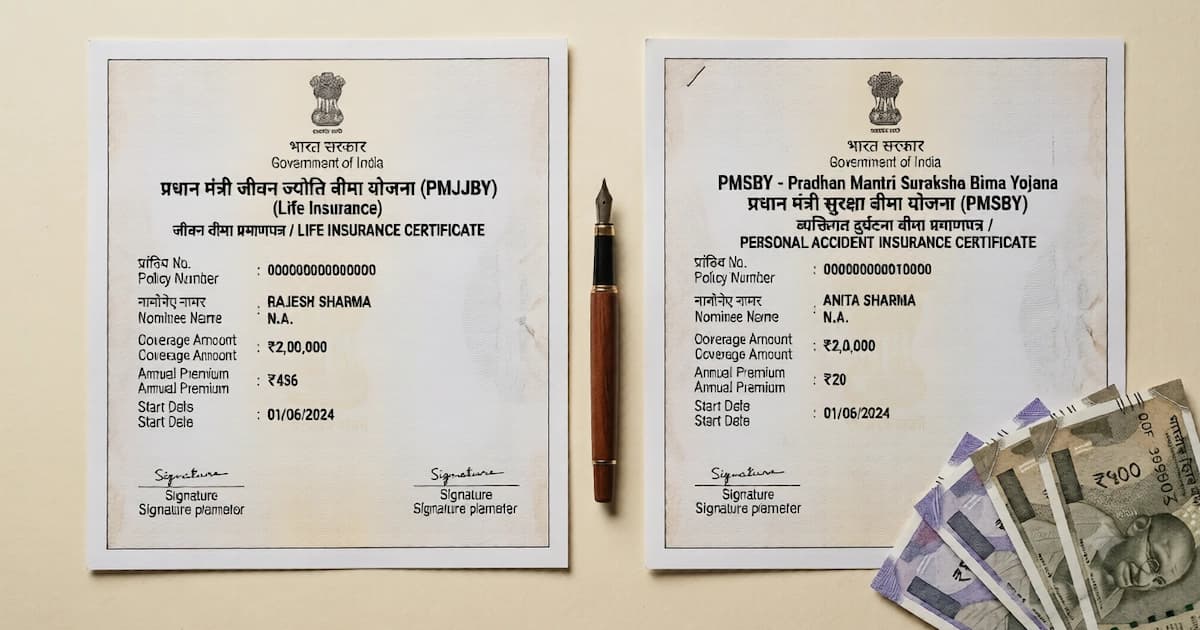

PMJJBY vs PMSBY: Rs 436/yr for Rs 2 lakh life cover vs Rs 20/yr for Rs 2 lakh accident cover. Age limits, the 30-day lien, claims, and holding both for Rs 456.

14 min read

NSC pays 7.7% with an 80C tax break; KVP pays 7.5% and doubles your money in 115 months. Current Jul-Sep 2026 rates, tax, and a worked comparison.

12 min read

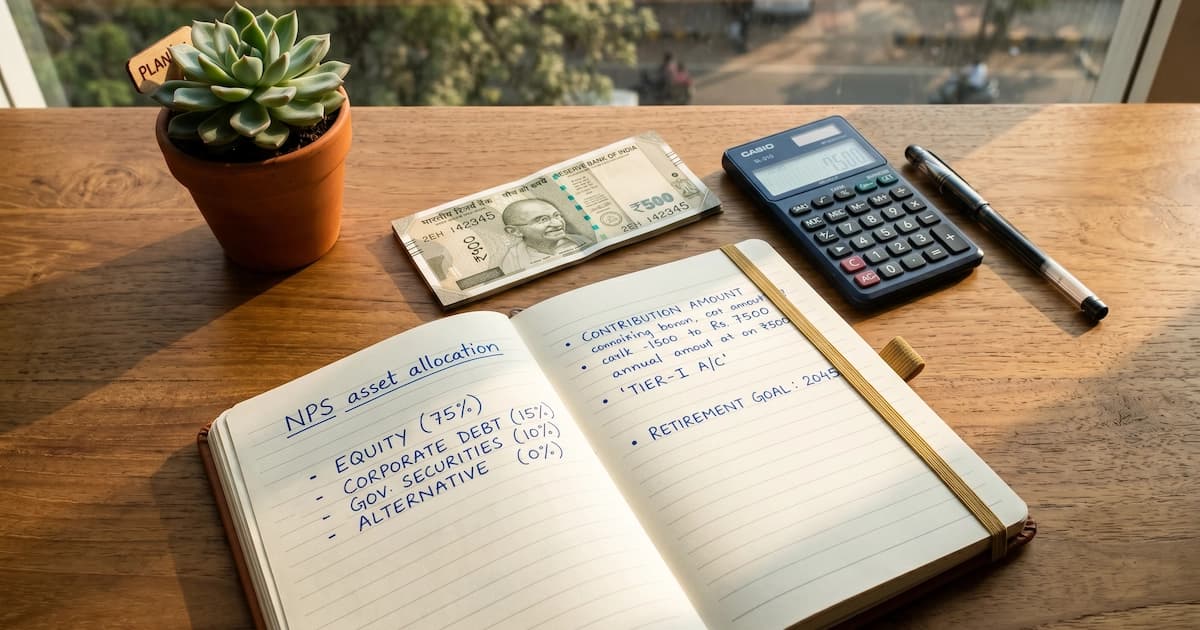

What is NPS (National Pension System)? Tier I vs Tier II, equity/debt/government asset choices, Section 80CCD(1B) extra ₹50K deduction, and the 60% lump sum + 40% annuity rule at retirement.

9 min read

What is EPF (Employee Provident Fund)? The 8.25% interest rate, mandatory 12%+12% employee/employer contribution, EPS split, withdrawal rules, and tax treatment explained for salaried Indian workers.

9 min read

What is Atal Pension Yojana? The guaranteed monthly pension of ₹1,000-₹5,000 at age 60, eligibility for unorganized-sector workers aged 18-40, monthly contribution table, and how APY differs from NPS.

9 min read

YNAB vs Mint comparison updated for 2026, covers the March 2024 Mint shutdown, what the YNAB vs Mint trade-offs were, and the best Mint replacements (Monarch, Empower, Rocket Money) for former Mint users.

8 min read

Researched guide to legitimate work from home jobs for beginners in 2026, entry-level remote roles, real salary ranges, verified job boards, and how to spot the scam patterns that dominate WFH search results.

9 min read

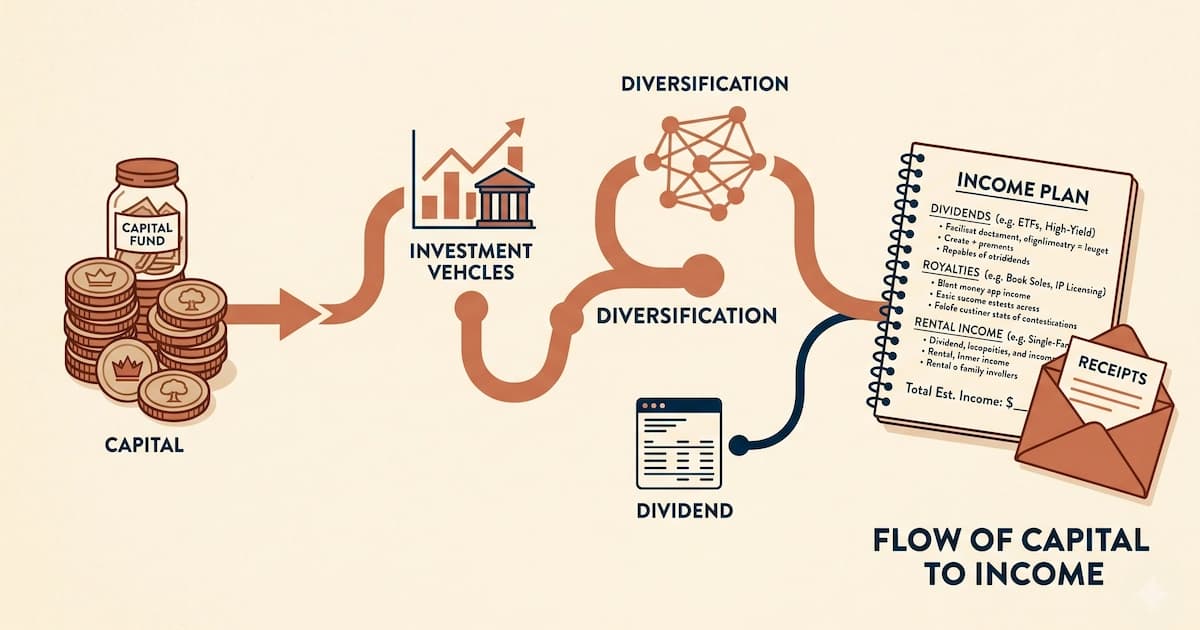

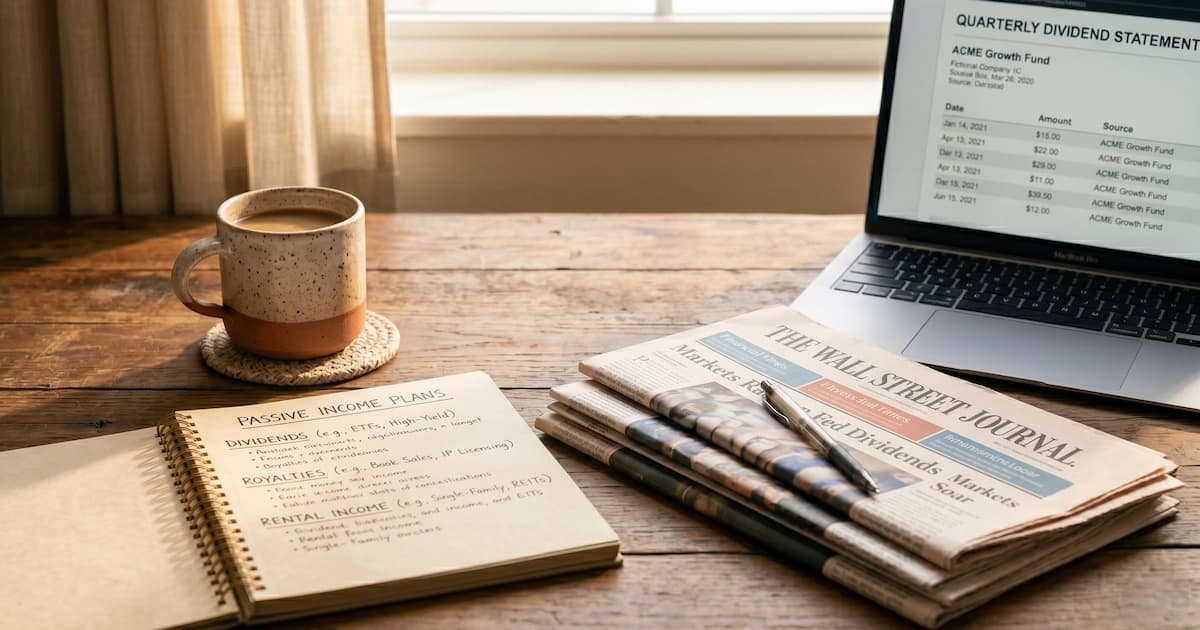

What is passive income? The IRS legal definition, the everyday financial definition, how it differs from active and portfolio income, and what actually qualifies as passive vs what just gets marketed that way.

8 min read

Researched list of side hustles that require zero upfront capital, freelance writing, virtual assistance, tutoring, content creation. Honest timelines and earnings expectations for India and US.

8 min read

Researched list of side hustles that suit introverts, writing, design, programming, transcription, data labelling. Filtered for async work, minimal real-time interaction, and written-first communication.

8 min read

Honest researched guide to passive income for beginners, distinguishes truly passive (capital + royalties) from semi-passive (content, courses) from misleadingly-labelled passive (most influencer pitches). India and US specifics.

9 min read

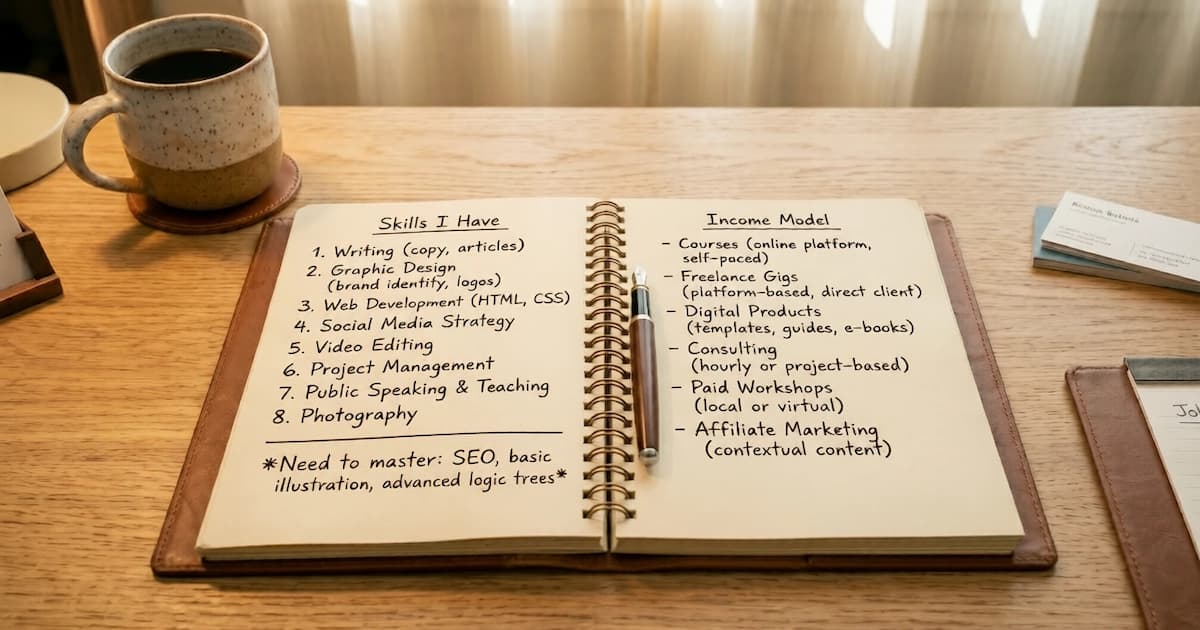

Researched framework for identifying skills you can monetize and matching them to the right income model, freelance services, courses, products, consulting, and content. India and US specifics.

9 min read

Researched guide for students looking to make money online in 2026, best beginner-friendly income sources for limited time, no professional experience, and college schedules. India and US specifics.

9 min read

Complete beginner guide to YNAB (You Need A Budget), the four rules explained, account setup, category structure, first-month workflow, and the gotchas most new users hit.

9 min read

Researched guide to negotiating your salary on a new job offer, market rate research, the negotiation conversation framework, what's negotiable beyond base salary, and India + US specifics for CTC, equity, and benefits.

9 min read

Researched guide to asking for a raise, when to time the request, how to document your value, the conversation framework, and what to do if denied. India and US specifics including annual cycle vs market-adjustment requests.

9 min read

Plain-English explainer on the gig economy in 2026, what gig work means, the major platforms by category, employee vs contractor classification, tax implications, and India and US regulatory frameworks.

9 min read

Researched guide to starting freelancing as a beginner in 2026, the 5 freelance categories, platforms vs direct clients, pricing your work, contracts and invoicing, and tax obligations in India and US.

10 min read

The best beginner side hustles for 2026 with realistic ₹ and $ earnings, startup cost, time to first payment, and how side income is taxed in India and the US.

16 min read

Researched list of the best personal finance podcasts for 2026, covering The Ramsey Show, Planet Money, ChooseFI, BiggerPockets Money plus Indian shows like Paisa Vaisa and Capitalmind.

8 min read

Researched comparison of the best investment tracking apps for 2026, Sharesight, Empower, Morningstar, Kuvera, Groww, INDmoney plus CoinTracker and Koinly for crypto. India and US markets.

9 min read

The best finance and stock-market YouTube channels in India and the US for 2026: Rachana Ranade, Pranjal Kamra, Graham Stephan, Ben Felix, and who each one is for.

14 min read

The best personal finance books for beginners in India and the US: Let's Talk Money, The Psychology of Money, Coffee Can Investing, and a reading order.

13 min read

Best expense tracker apps for 2026: US (Rocket Money, Monarch, Empower) and India (Moneyview, axio, ET Money), free and paid, plus the SMS-tracking reality.

14 min read

The best budgeting apps for college students in 2026, including YNAB's free student offer, Splitwise for shared expenses, and free Indian and US options that fit student budgets.

8 min read

Researched comparison of the best budgeting apps for beginners in 2026, YNAB, Monarch, Goodbudget, Empower, ET Money, Jupiter and more. Free vs paid, India vs US, and how to pick one.

9 min read

Compare the 8 best net worth tracker apps for 2026, free and paid. Empower, Monarch, Kubera, with pricing, best-for picks and a Mint alternative.

14 min read

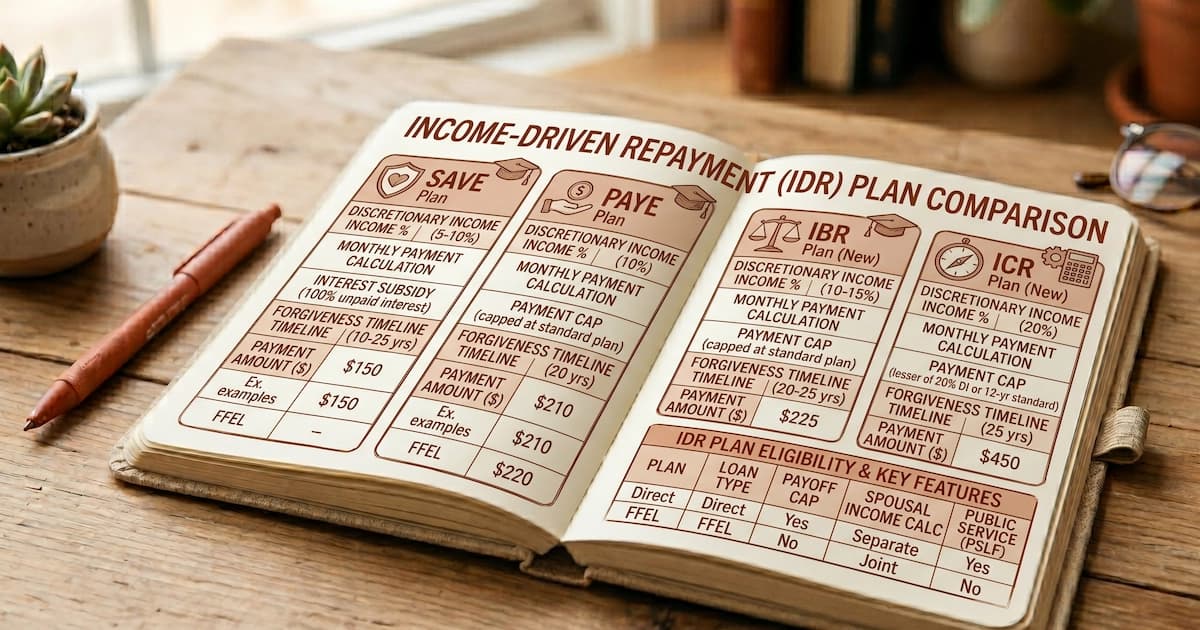

What is income-driven repayment, a clear breakdown of SAVE, PAYE, IBR, and ICR, the discretionary income formula, the 20- or 25-year forgiveness clock, and what India offers instead.

9 min read

What is a high-yield savings account? A plain-English explanation of how HYSAs work, why their rates are so much higher than traditional bank savings accounts, what to look for, and how to choose one.

9 min read

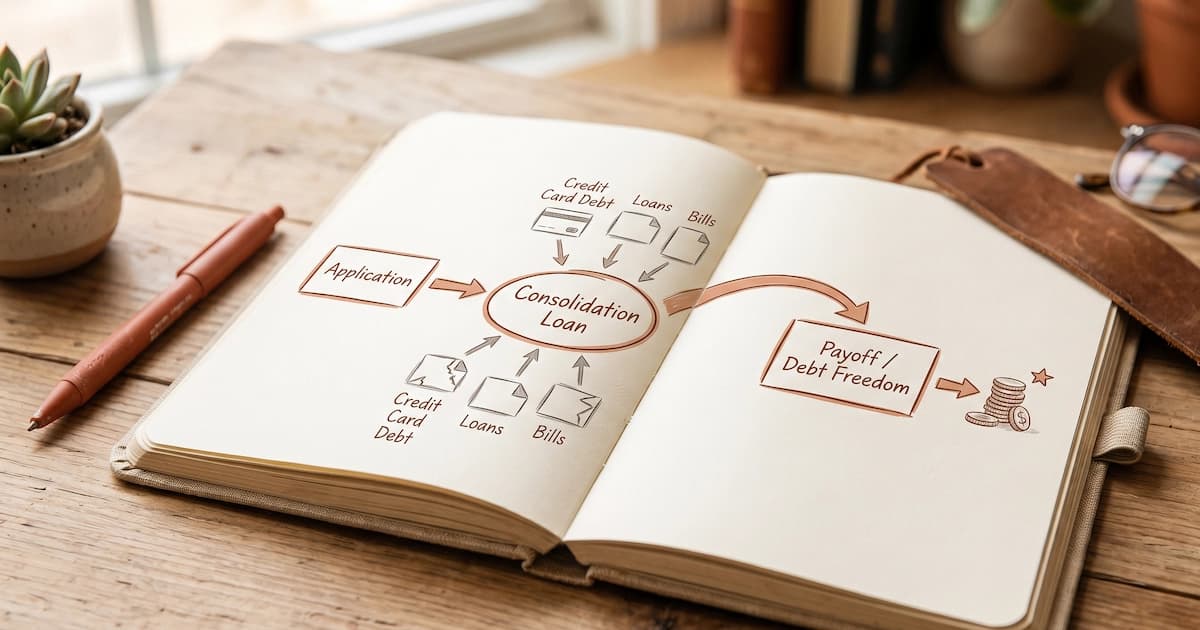

What is a debt consolidation loan, the three main forms it takes in India and the US, and the conditions under which it actually saves money instead of just rearranging it.

9 min read

A good credit utilization ratio is under 30%, and top scores sit under 10%. Why 30% is not an official FICO or CIBIL rule, and how to lower yours fast.

13 min read

What is an emergency fund? A plain-English definition of the savings category that exists separately from goals and investments, and why it's the foundation every other financial decision sits on top of.

8 min read

What is a sinking fund? A plain-English definition of the savings category designed for known future expenses, and why personal finance educators describe it as the missing layer between budgeting and emergency funds.

8 min read

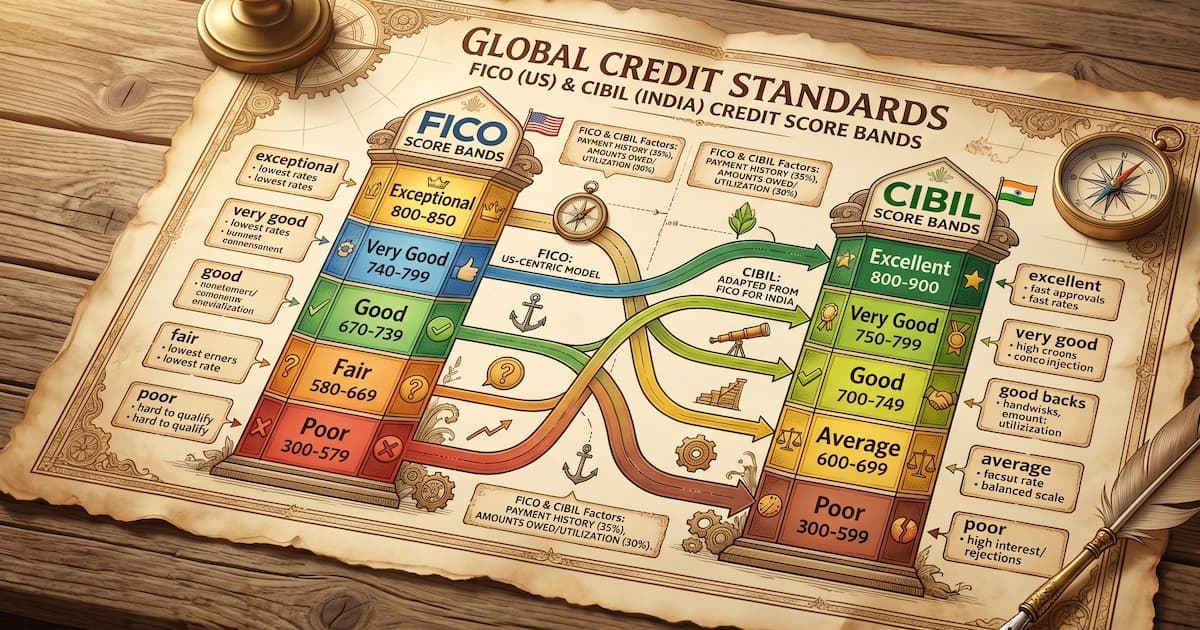

A good credit score is 670+ on FICO (max 850) and 750+ on CIBIL (max 900). See every band, what each one unlocks, and what a good score really saves you.

12 min read

What happens if you don't pay credit card debt? The 30/60/90/180-day delinquency timeline, late fees, penalty APR, credit score damage, charge-off, collections, and lawsuit risk in India and US.

9 min read

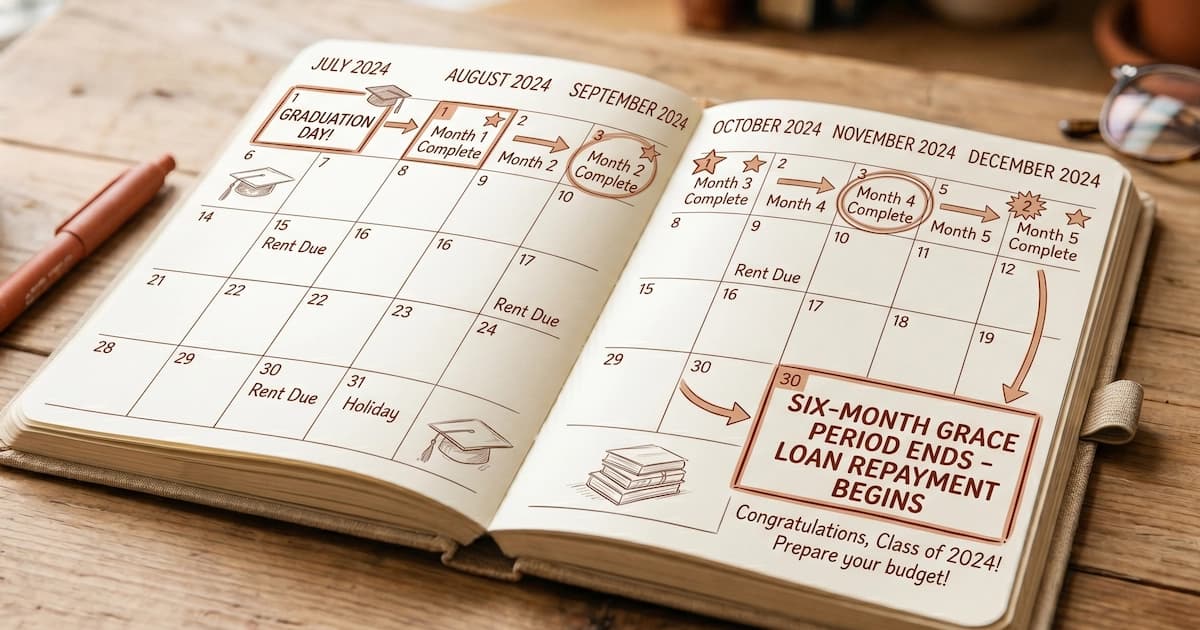

The student loan grace period explained, six months on US federal loans, course duration plus 6-12 months in India, with the interest accrual rules that decide what you actually owe.

8 min read

Sinking fund vs emergency fund, the two savings categories serve different jobs, and mixing them often produces households that 'have savings' but stay financially fragile. Direct comparison with examples.

8 min read

Savings account vs checking account, how the two account types differ, why most households need both, and how to set up the structural separation that makes saving easier.

8 min read

How to save money on a tight budget, the structural tactics that actually work for households living close to the line, not the generic 'cut your latte' advice that doesn't survive the first hard week.

9 min read

Best ways to save money as a student, the categories where the gains are biggest (housing, food, textbooks, transport), the social pressure that defeats most plans, and the habits that pay off long after graduation.

9 min read

How to save for a house down payment, picking the right target percentage, choosing the right account type, and working out a realistic timeline based on your income and the local market.

9 min read

Money saving tips for beginners, twelve tactics organised by leverage, from the structural moves that produce the biggest gains to the small habits that compound over time.

9 min read

How to save money every month, the structural system that produces consistent monthly savings without relying on willpower or month-end leftover. The transfer order, the buffer, and the categories worth automating.

9 min read

How to cut expenses without feeling deprived, the structural cuts that don't require willpower, the discretionary cuts that target low-value spending without removing the high-value spending, and how to avoid the rebound month that wipes out the savings.

8 min read

How to build an emergency fund from scratch, the four-stage path from $0 to a fully-funded six-month buffer, and what to do at each stage when life interrupts.

9 min read

How student loan interest works in plain English, daily simple interest accrual, capitalisation rules, and the actual rates on US federal loans and Indian education loans for 2024-25.

9 min read

How much emergency fund do you need? A method for picking your specific target amount based on your essential expenses, income stability, and household situation, not a generic 3-to-6-month rule.

8 min read

How long does it take to pay off credit card debt? Worked examples comparing minimum payments, fixed monthly payments, and avalanche/snowball methods, in both rupees and dollars.

9 min read

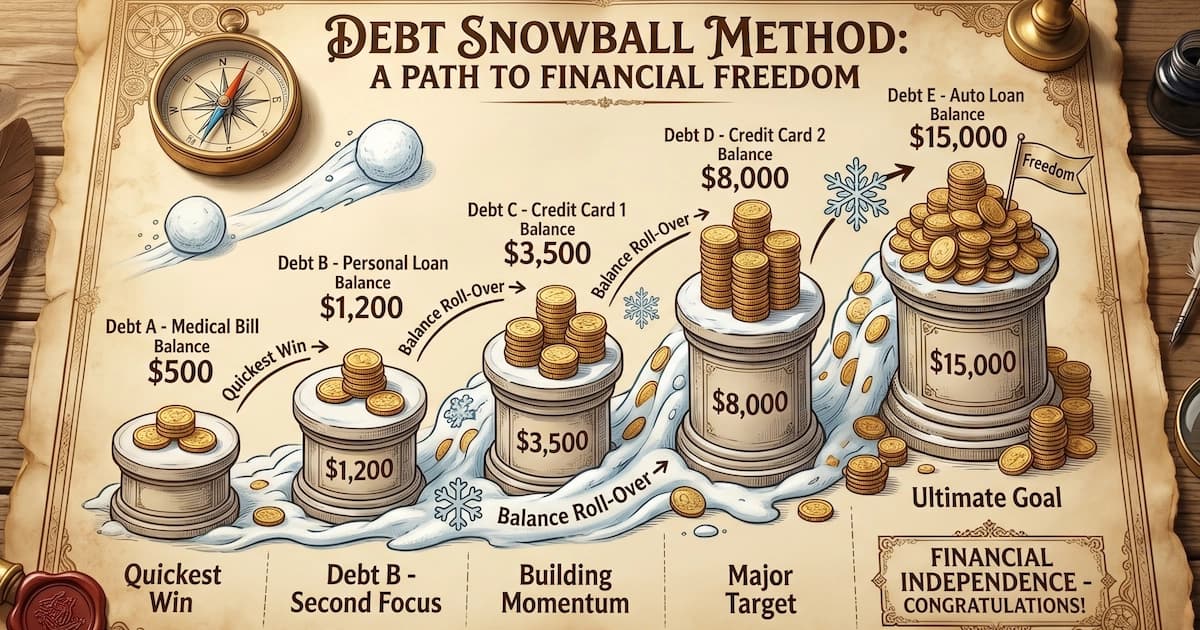

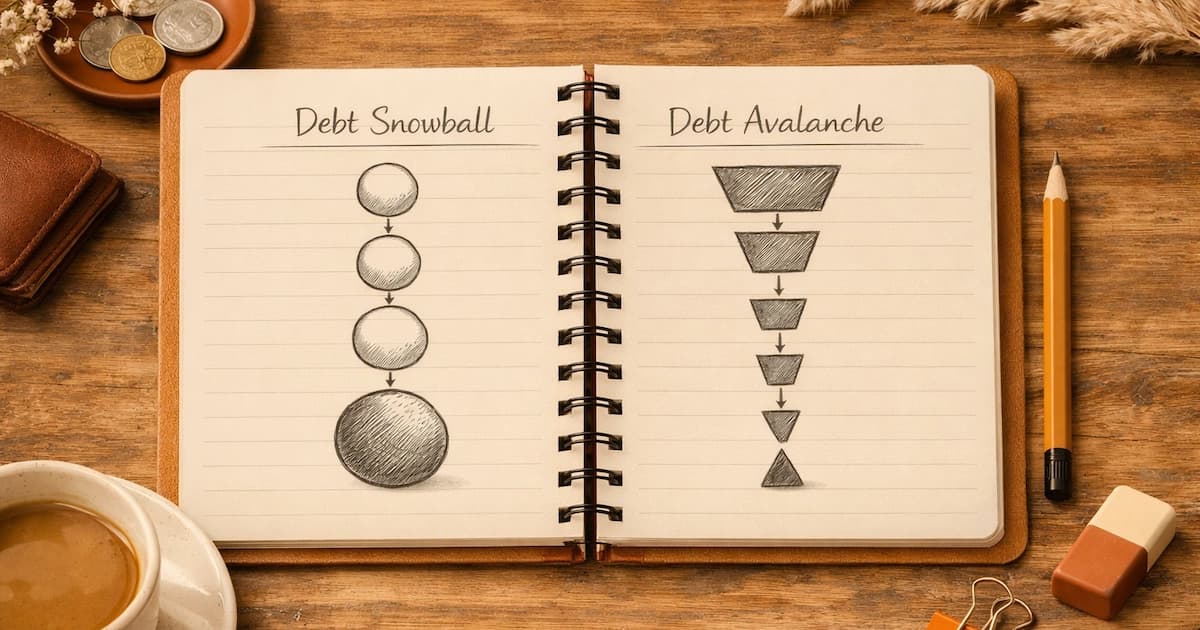

How the debt snowball method works, step by step: pay the smallest balance first, roll each payment forward, and stay motivated. Worked payoff examples in ₹ and $.

13 min read

How does debt consolidation work in practice, the application, qualification, funding, payoff, and credit-score sequence, with a worked example showing the interest-savings math.

9 min read

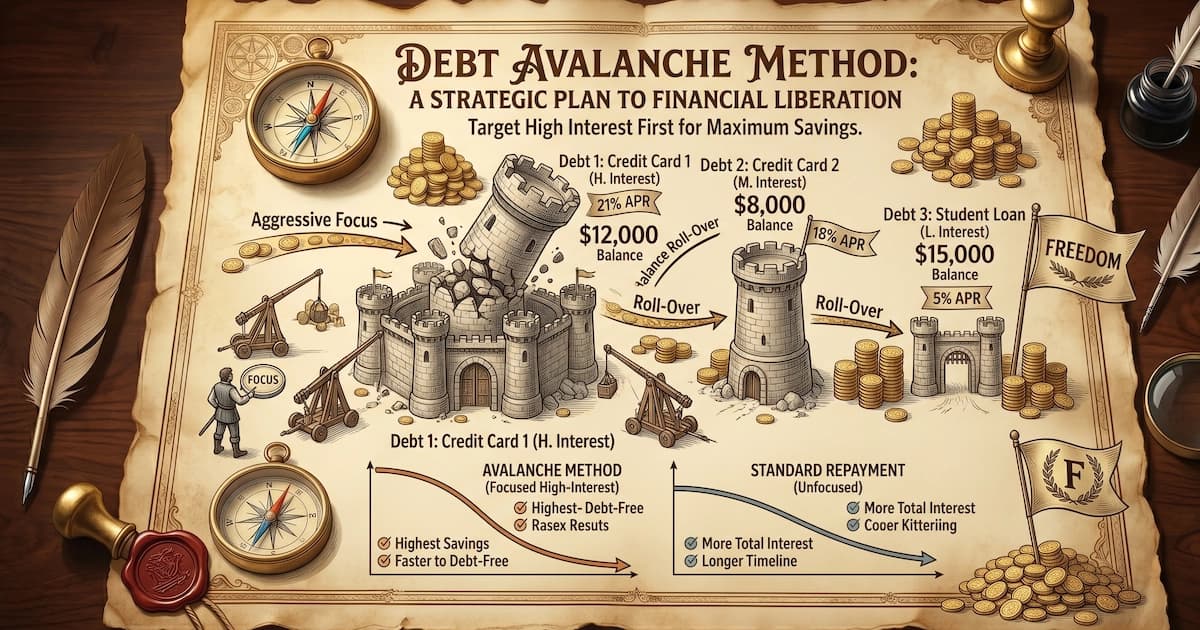

How the debt avalanche method works, the math on how much it saves vs the snowball, worked examples in rupees and dollars, and when avalanche is the right choice.

9 min read

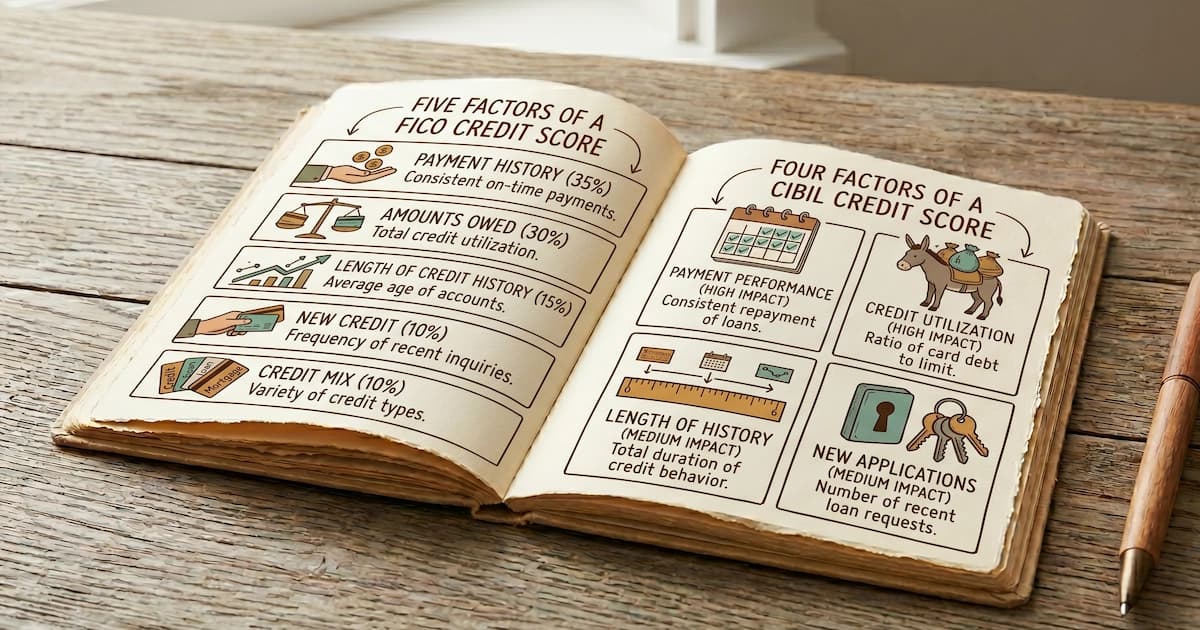

How credit scores are calculated by FICO in the US (5 factors) and TransUnion CIBIL in India (4 factors), with the exact weights and what each one measures.

9 min read

Credit card interest is charged daily on your average daily balance once you carry a balance. The real math, grace periods, and the minimum trap, in ₹ and $.

13 min read

Why budgeting is important, the research findings on financial well-being, the structural reasons budgets work even when willpower doesn't, and the long-term costs of not having one.

9 min read

Zero-based budgeting gives every dollar a job until income minus spending equals zero. The 5 steps, a worked $ and Rs example, pros and cons, and a free template.

13 min read

The pay yourself first method explained. Where the idea comes from, how to set up automatic transfers, and why prioritising savings before expenses changes the math.

8 min read

What is a no-spend challenge? The rules, the categories that count as essentials versus discretionary, the benefits beyond the savings amount, and the rebound trap that catches most participants.

8 min read

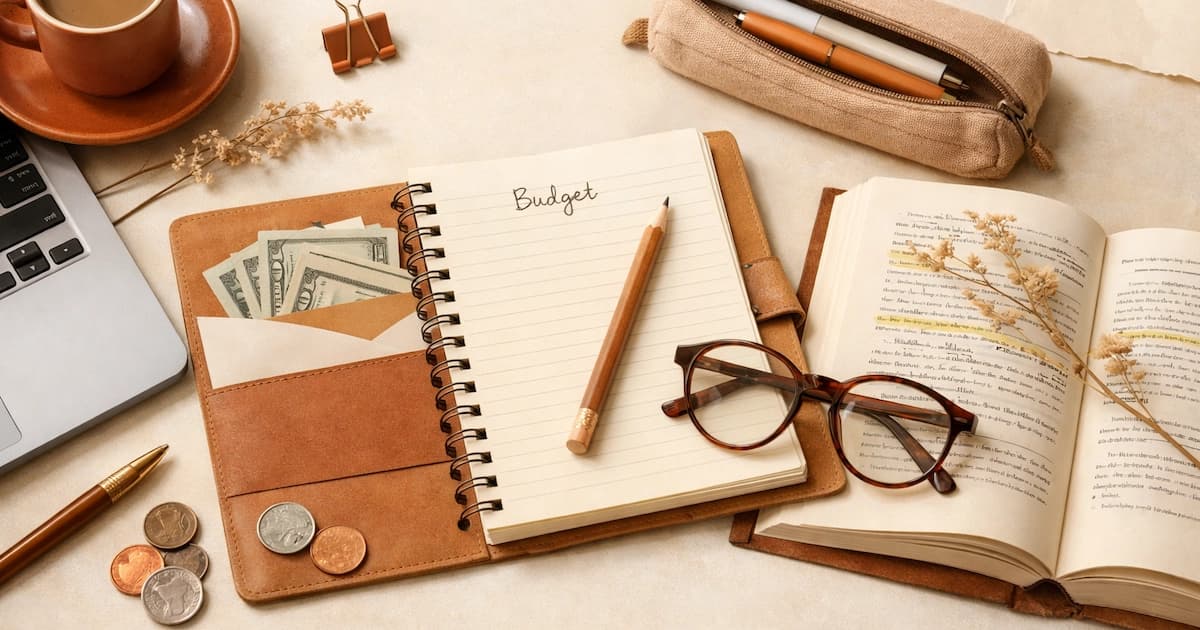

A simple monthly budget template for beginners, what categories to include, what amounts to assign, and a worked example you can copy directly into a spreadsheet, app, or notebook.

9 min read

Money saving challenges for 2026, ten popular challenges, who each one suits best, and the structural reason short-term challenges work even when long-term resolutions fail.

9 min read

How to track your spending, the four common methods (apps, spreadsheets, notebooks, receipts), how to choose one, and the routine that turns tracking into a sustainable habit.

9 min read

How to make a budget for the first time, step by step. Gathering the information you need, choosing categories, picking a method, and the routine that turns a one-time setup into a habit.

9 min read

What is the envelope budgeting method? The cash-envelope system explained, how to set it up, the digital alternatives, and where it works (and doesn't).

9 min read

Debt snowball vs avalanche method compared, how each works, the math on which saves more money, the behavioural research on which one people actually finish, and how to choose.

9 min read

Budgeting tips for single moms, handling childcare, irregular co-parent contributions, the emergency fund that absorbs sole-provider risk, and the benefits and tax credits worth knowing about.

9 min read

Budgeting tips for college and university students, handling tuition, low and irregular income, textbook costs, and the financial habits that pay off long after graduation.

9 min read

Budgeting tips for freelancers and self-employed workers, handling variable monthly income, quarterly taxes, the irregular invoice timing, and the buffer that prevents lean months from becoming crises.

9 min read

Twelve practical budgeting tips for beginners, what to do in week one, how to avoid the common collapse points, and the small habits that determine whether a budget survives month two.

9 min read

Build a budget in Google Sheets step by step: the exact columns, the SUM and SUMIF formulas, conditional formatting, and a free template to copy, in ₹ or $.

14 min read

The 52-week money saving challenge explained. The standard rules, why the math works out to $1,378, the common variations, and how to keep going past month nine when most people drop off.

8 min read

The 50/30/20 rule of budgeting explained in plain English. Where the rule came from, how to calculate the three buckets, and when it works (and when it doesn't).

9 min read

What is the FIRE movement? A plain-English explanation of Financial Independence Retire Early, the math, the variants, and the trade-offs of the FIRE framework.

8 min read

What does financial freedom mean? A plain-English definition, the levels people commonly talk about, and what the term actually requires in practical terms.

7 min read

What is diversification? A plain-English explanation of how spreading investments reduces risk, the different ways to diversify, and why the concept gets discussed so often.

8 min read

What is compound interest? A plain-English explanation of how interest builds on itself, why time matters more than rate, and how it works on both savings and debt.

8 min read

What is a W-2 form? A plain-English explanation of the U.S. tax form your employer issues each January, what each box means, and how it gets used at tax time.

8 min read

What is a credit report? A plain-English explanation of what's on it, where it comes from, who can see it, and how it differs from a credit score.

8 min read

What is a 1099 form? A plain-English explanation of the U.S. tax forms used to report non-employee income, freelance, gig, interest, dividends, and more.

8 min read

What are taxes actually used for? A plain-English breakdown of where federal, state, and local tax dollars go, and why understanding this matters for personal finance.

8 min read

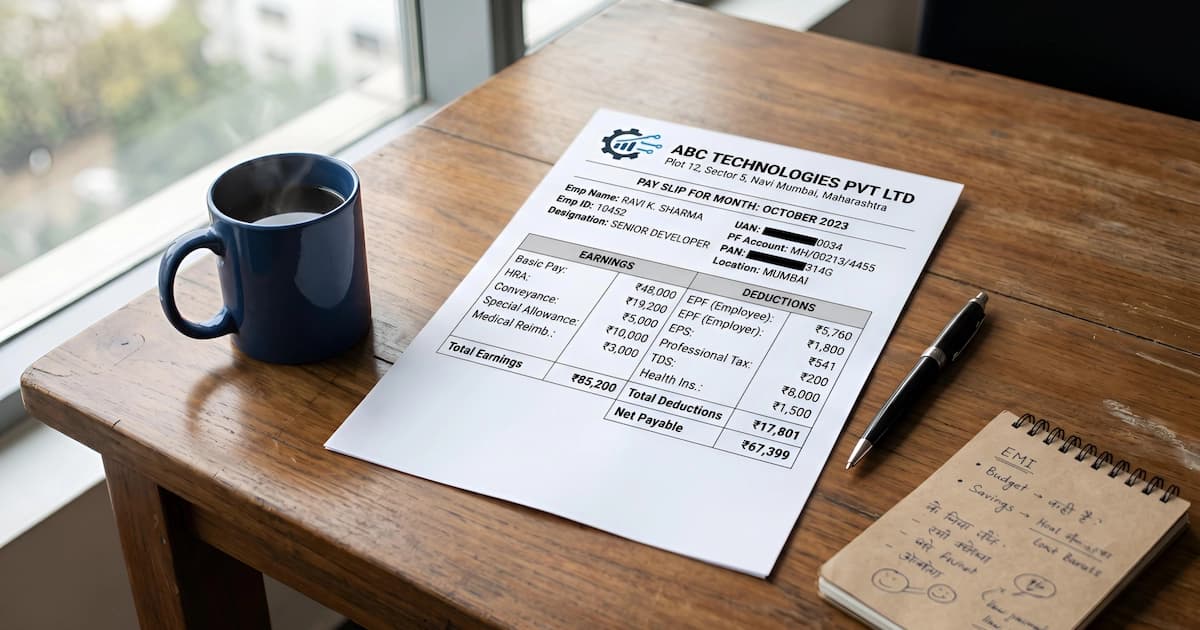

How to read a pay stub: a plain-English walkthrough of every line item, from gross pay to deductions to net take-home, plus the year-to-date totals that matter at tax time.

8 min read

Difference between gross and net income, in plain English. What gets deducted, why the gap exists, and which number to budget against in real life.

7 min read

What is an interest rate? A plain-English explanation of how interest works, how it is calculated, and why the same number behaves differently in different contexts.

8 min read

What is the difference between APR and interest rate? A plain-English explanation of why they differ, what APR includes, and which to compare when shopping for a loan.

8 min read

How does inflation affect your money? A plain-English breakdown of what inflation does to savings, wages, debt, investments, and long-term goals.

9 min read

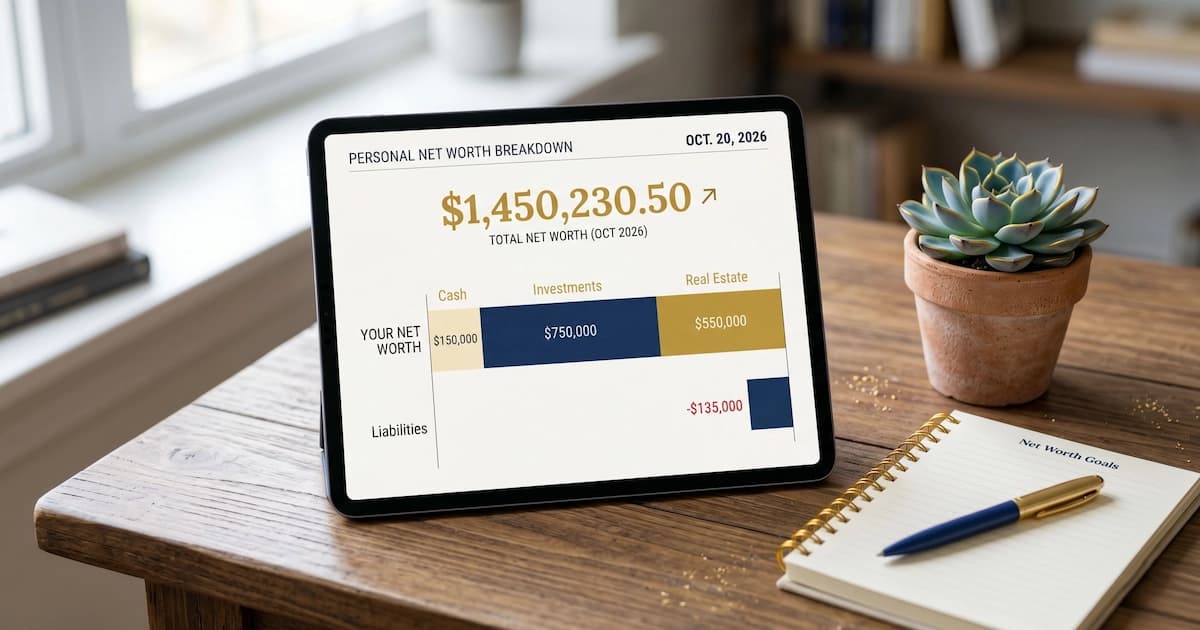

What is net worth? A plain-English explanation of the most foundational personal finance number, plus how to calculate yours in five minutes.

8 min read

What is inflation? A plain-English explanation of how prices rise, how it is measured, and what it actually means for everyday savings, wages, and debt.

9 min read

Common financial terms explained in plain English: income, interest, APR, credit utilization, net worth, and more. A beginner's glossary, no jargon.

9 min read

What is financial literacy? A plain-English explanation of the skill that helps people make informed money decisions. No jargon, no advice, just clear research.

8 min read

Personal finance basics explained in plain English: income, saving, debt, credit, and investing, the small set of concepts every adult tends to encounter.

8 min read