How Does the Debt Snowball Method Work? Steps + Examples

By Tapabrata Biswas · Updated July 4, 2026 · 13 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

The debt snowball method is a payoff plan where you clear your debts from the smallest balance to the largest, ignoring interest rates, and roll each freed-up payment into the next debt so it grows like a snowball rolling downhill. It is the most popular debt-payoff method in the world, and the interesting thing about it is that it is deliberately not the cheapest one. It trades a little bit of maths for a lot of motivation, and for most people that trade is what actually gets them out of debt.

A 2012 study by researchers at Northwestern University's Kellogg School of Management found that people who paid off their smallest debt first were more likely to eliminate their entire balance than people who paid off the highest-interest debt first. The mathematically optimal plan was the one more people quit. That single finding is the whole case for the snowball: behaviour, not arithmetic, is the binding constraint on getting out of debt.

What is the debt snowball method?

The debt snowball method is a debt-payoff strategy where you pay your debts in order of smallest balance to largest, regardless of interest rate, rolling each cleared debt's payment into the next one to build momentum. You pay the minimum on every debt, throw all your spare money at the smallest balance until it is gone, then send that freed-up payment to the next-smallest debt, and so on.

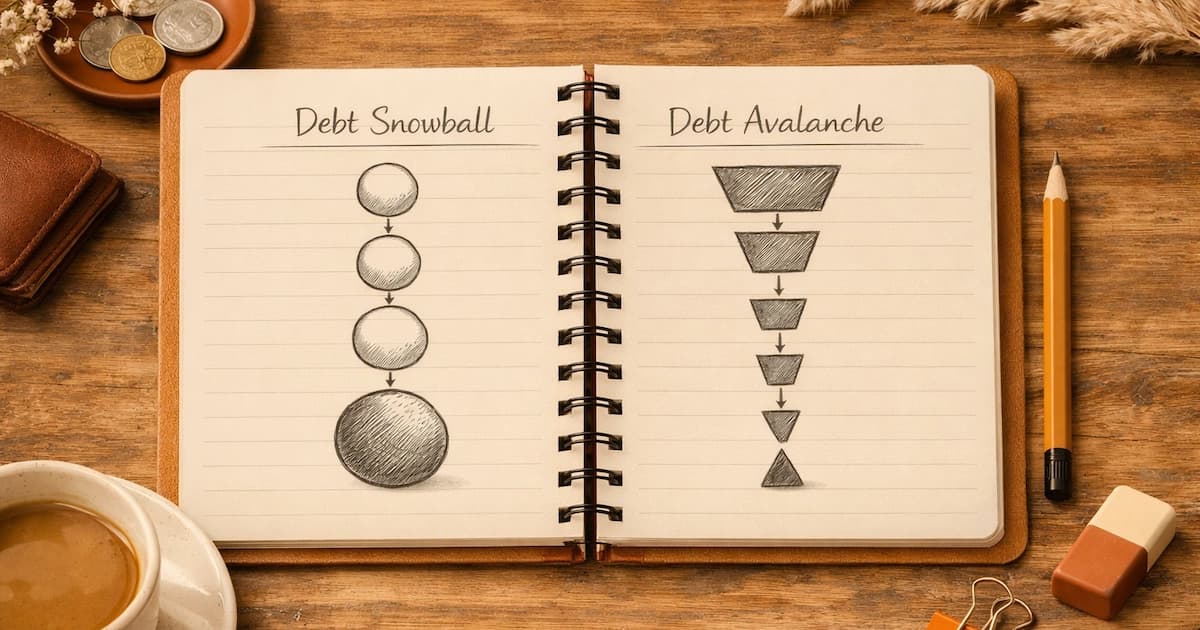

Dave Ramsey popularised the method and made it Baby Step 2 of his plan, though the underlying idea of starting small for momentum is older. It is one of two dominant ways to order debt payoff. The other, the avalanche method, goes highest interest rate first. The two produce a different order unless your smallest debt also happens to carry the highest rate, which is uncommon.

The appeal of the snowball is psychological. By hitting the smallest balance first, you close an entire account early, often within 60 to 90 days, and that visible win creates the motivation to keep going for the two to four years a full payoff usually takes.

How the debt snowball works, step by step

- List every debt by balance, smallest to largest: name, balance, minimum payment, and rate. Leave your mortgage off the list.

- Add up your total monthly debt budget. Sum all the minimums, then add whatever extra you can afford above them. This total stays the same for the whole payoff.

- Attack the smallest balance. Pay the minimum on everything else, and put the smallest debt's minimum plus all your extra onto it until it clears, usually in one to three months.

- Roll the payment forward. When the smallest debt is gone, its old minimum plus your extra now goes to the next-smallest debt. Your total monthly payment does not change, only where it lands.

- Repeat down the list until the largest debt is paid.

- Track it where you can see it. A debt thermometer or a spreadsheet that fills in as balances fall keeps the motivation alive, and the people who finish almost always track visibly rather than just letting auto-pay run.

Worked example in dollars

Take a US household with these four debts, an extra $300 a month above minimums, and $400 in total minimums, so a fixed $700 a month goes to debt.

| Order | Debt | Balance | APR | Min | Snowball payment | Clears around |

|---|---|---|---|---|---|---|

| 1 | Medical bill | $450 | 0% | $25 | $325 | month 2 |

| 2 | Store credit card | $1,200 | 26% | $35 | $360 | month 6 |

| 3 | Personal loan | $4,500 | 11% | $120 | $480 | month 17 |

| 4 | Auto loan | $9,800 | 7% | $220 | $700 | month 37 |

Watch the snowball payment column grow: $325, then $360, then $480, then the full $700, because each cleared debt hands its payment to the next. Two of the four accounts close inside the first half-year, which is the visible-win pattern the method runs on. Total timeline is roughly 37 months, and total interest is about $2,400.

Now the honest part almost no guide shows. Run the exact same four debts under the avalanche method (highest rate first: the 26% store card, then the 11% personal loan, then the 7% auto loan, then the 0% medical bill) and you would pay roughly $200 to $300 less in interest and finish about a month sooner. That gap is the price of the snowball's early wins. For a mix like this it is small, which is exactly why so many people choose the motivation.

Worked example in rupees

Take an Indian household with these debts, an extra ₹8,000 a month above minimums, and ₹13,300 in total minimums, so a fixed ₹21,300 a month goes to debt.

| Order | Debt | Balance | APR | Min | Snowball payment | Clears around |

|---|---|---|---|---|---|---|

| 1 | Buy-now-pay-later | ₹8,000 | 0% promo | ₹1,500 | ₹9,500 | month 1 |

| 2 | Credit card | ₹35,000 | 39% | ₹3,500 | ₹13,000 | month 4 |

| 3 | Two-wheeler loan | ₹65,000 | 11% | ₹2,800 | ₹15,800 | month 12 |

| 4 | Personal loan | ₹1,80,000 | 14% | ₹5,500 | ₹21,300 | month 28 |

The BNPL clears in the first month, the credit card a few months later, and the payment keeps snowballing until the personal loan gets the entire ₹21,300. Total timeline is roughly 28 months, and total interest is about ₹56,000.

Notice the snowball pays the 0% BNPL before the 39% credit card, purely because the BNPL balance is smaller. An avalanche would hit the 39% card first and save you a few thousand rupees in interest. Indian credit cards commonly charge 36% to 42% a year, so if a large card balance is your biggest cost, the avalanche gap is worth weighing. For smaller, mixed balances like this one, the early BNPL and card wins usually matter more than the small saving.

Why the debt snowball works: the psychology

The snowball beats the maths on completion because of how progress feels. A 2012 study by Gal and McShane at Northwestern Kellogg, published in the Journal of Marketing Research, found that closing out individual debt accounts one at a time predicted getting fully out of debt better than optimising total interest did. The same authors popularised the idea in a 2016 Harvard Business Review piece called "The Small-Victories Strategy for Paying Off Debts."

There is a related finding worth knowing. In a 2011 Journal of Marketing Research paper, "Winning the Battle but Losing the War," Amar and colleagues described "debt account aversion," the tendency to want fewer open debts even when concentrating on the highest rate would save money. The snowball works with that instinct instead of against it: it gives you fewer accounts fast, which feels like winning and keeps you in the game.

The practical takeaway is simple. The snowball is not mathematically optimal, but it is behaviourally optimal for a lot of people, and a finished snowball saves far more than an avalanche you abandon at month nine.

Debt snowball vs avalanche, in brief

The avalanche method orders debts by interest rate, highest first, so it always pays the least total interest. The snowball orders by balance, smallest first, so it usually delivers the first cleared account soonest. On typical consumer mixes the interest difference is modest, often $100 to $500, and it widens when you have one large high-rate debt. Choose the avalanche if the numbers motivate you and your highest-rate balance is big; choose the snowball if quick wins keep you going.

That is the short version. For the full side-by-side, with the same debts run both ways and the exact interest and timeline difference, see our dedicated guide on debt snowball vs avalanche, and for the other method's mechanics, how the debt avalanche method works. To run your own debts through both methods and see which clears them faster and cheaper, use our debt snowball vs avalanche calculator.

When the snowball is the right choice

The snowball tends to fit three situations. First, people who have quit a payoff plan before: if an earlier avalanche stalled because the big high-rate debt would not visibly move, the snowball's faster wins are worth the small premium. Second, people with several small debts mixed in with larger ones, since those little balances clear in the first few months and cut the mental clutter. Third, people whose debts are all at similar rates, where the avalanche's maths advantage is tiny anyway.

There are moments to pause the snowball too: an income shock, a genuine emergency with no cash buffer, or a 0% promotional window that is about to expire on one card. Outside those, the method rewards consistency.

What the snowball needs to work

Four things make or break it: a budget that protects the debt-payoff line, stopping new charges on the cards you are paying down, a small starter emergency fund (about $1,000, or roughly ₹50,000) so a surprise expense does not send you back to the cards, and patience for a 24-to-48 month timeline. Our guide on how to build an emergency fund covers that starter cushion. To model the total cost and payoff time of any single debt, our loan calculator compares interest across three tenures.

Common mistakes

The usual failures are avoidable. Skipping visible tracking removes the motivation the method depends on. Not rolling the freed-up payment forward, and letting it drift back into spending, quietly adds months. Switching between snowball and avalanche mid-way scrambles your order and your mental picture. And the most common killer of any payoff plan is charging the cards back up while paying them down, so the cards stay cold until the last balance is gone.

Frequently asked questions

How does the debt snowball method work? List every debt from smallest balance to largest, ignoring interest rates. Pay the minimum on every debt except the smallest, and put all your extra money toward the smallest until it is gone. When it clears, roll its old minimum plus your extra into the next-smallest debt, and repeat. The snowball is that monthly payment growing bigger as each debt closes.

Does the debt snowball save money compared to the avalanche? No, the avalanche usually saves more interest because it targets the highest rate first, but the gap is often small, roughly $100 to $500 for a typical mix. The snowball trades that for early wins that keep people going, and a finished snowball beats an abandoned avalanche. If your highest-rate debt is large, the avalanche gap grows and is worth weighing.

Does the debt snowball include my mortgage? No. The snowball is for consumer debts: credit cards, personal loans, BNPL, car and two-wheeler loans, student loans, and medical bills. Your home loan is left out, since it is far larger and is long-term secured debt rather than the high-cost consumer debt the method is built to clear.

How long does the debt snowball typically take? For $10,000 to $25,000 of mixed consumer debt and an extra $300 to $500 a month, the usual timeline is 24 to 48 months. Smaller balances often finish in under two years; $40,000-plus takes three to five. The first debt usually disappears in the first 60 to 90 days.

Why does the snowball work when the avalanche saves more money? Because payoff is a behaviour problem. Closing a whole account early gives a visible win and momentum that carry people through a multi-year payoff. The 2012 Kellogg study by Gal and McShane found smallest-balance-first predicted full payoff better than optimising interest. The best method is the one you finish.

What if my smallest debt has the lowest interest rate? That is the normal case, and the method still says pay it first. The extra cost is small, usually $100 to $500. If the rate gap is extreme, many people snowball the tiny debts, then switch to avalanche for the rest.

In summary

The debt snowball method orders your debts from smallest balance to largest, sends all your spare money to the smallest until it closes, then rolls that payment forward to the next debt. It is not the cheapest method, the avalanche usually saves a little more interest, but it is the one more people finish, because the early closed accounts create the motivation a multi-year payoff needs. Leave your mortgage out, keep a small emergency fund so surprises do not send you back to the cards, and expect the first debt gone inside three months and the whole thing done in two to four years.

For the head-to-head numbers, see debt snowball vs avalanche, and for the other method on its own, how the debt avalanche method works.

Sources

- Gal and McShane, Can Small Victories Help Win the War? Evidence from Consumer Debt Management, Journal of Marketing Research, 2012 (Northwestern Kellogg)

- Gal and McShane, The Small-Victories Strategy for Paying Off Debts, Harvard Business Review, 2016

- Amar, Ariely, Ayal, Cryder and Rick, Winning the Battle but Losing the War: The Psychology of Debt Management, Journal of Marketing Research, 2011

- Ramsey Solutions, How the Debt Snowball Method Works: ramseysolutions.com

- Consumer Financial Protection Bureau, Debt management: consumerfinance.gov

You might also like

Debt snowball vs avalanche method compared, how each works, the math on which saves more money, the behavioural research on which one people actually finish, and how to choose.

9 min read

How the debt avalanche method works, the math on how much it saves vs the snowball, worked examples in rupees and dollars, and when avalanche is the right choice.

9 min read

What is the difference between APR and interest rate? A plain-English explanation of why they differ, what APR includes, and which to compare when shopping for a loan.

8 min read