What Is a Good Credit Score? FICO 850 & CIBIL 900 Bands

By Tapabrata Biswas · Updated July 8, 2026 · 12 min read

Researched with AI assistance, reviewed and edited by Tapabrata Biswas.

A good credit score is 670 or higher on FICO in the US and 750 or higher on CIBIL in India. Those are the thresholds where lenders stop treating you as a pricing risk and start offering their best published rates. The average American sits just below that line at a FICO of 713 (Experian, 2025), and the typical Indian borrower sits in the 650 to 699 band, so "good" is a level most people are close to but not quite at.

The more useful question buried inside "what is a good credit score" is: good enough for what? A 720 and a 760 both sound fine, yet on the same mortgage one qualifies for the loan and the other qualifies for the best rate on that loan, a gap worth tens of thousands over the term. This piece covers every band on both scales, why the ceilings differ (850 versus 900), and what a good score actually saves you in money.

What counts as a good credit score?

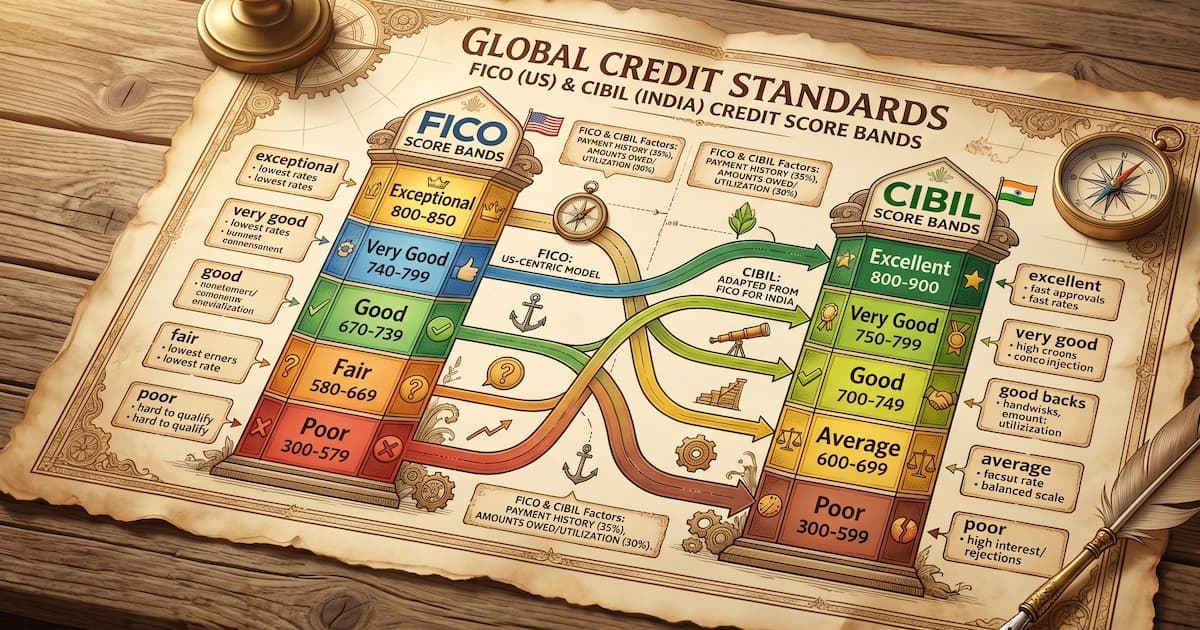

A good credit score is one high enough to unlock a lender's best published rates: 670-plus on FICO's 300 to 850 scale, and 750-plus on CIBIL's 300 to 900 scale. The two countries use different models with different maximums, so the same borrower would see two different numbers. Here they are side by side:

| Tier | FICO (US, 300 to 850) | CIBIL (India, 300 to 900) |

|---|---|---|

| Poor / entry | 300-579 | 300-649 |

| Fair | 580-669 | 650-699 |

| Good | 670-739 | 700-749 |

| Very good / lender-preferred | 740-799 | 750-799 |

| Top tier | 800-850 | 800-900 |

Read the table by row, not by number. A US "good" score of 700 and an Indian "good" score of 720 land in the same practical tier even though the raw numbers differ, because each is measured against a different ceiling. The one line worth memorising: in the US, 740-plus gets the best rates; in India, 750-plus does. Everything below those lines is a price penalty that grows the longer your loan runs.

CIBIL's scoring model is adapted from the FICO model, which is why the two behave so similarly in practice despite the different ranges. What "good" means is identical in both: enough credit history, paid on time, without leaning too hard on available limits.

FICO score ranges in the US

FICO publishes five bands on its 300 to 850 scale, and it powers roughly 90% of US lending decisions. The population shares below come from Experian's 2025 distribution data:

| FICO band | Range | Share of US consumers (2025) | What it unlocks |

|---|---|---|---|

| Poor | 300-579 | 14.7% | Most credit declined; secured cards and subprime products only |

| Fair | 580-669 | 14.9% | Some cards and auto loans approved at high rates |

| Good | 670-739 | 20.1% | Most mainstream credit at standard rates |

| Very Good | 740-799 | 27.5% | Best-advertised mortgage and auto rates open up |

| Exceptional | 800-850 | 22.8% | Premium rewards cards; lowest available rates |

About 70% of Americans now have a FICO of 670 or better, so most people already clear the good bar. The largest single band is very good (740 to 799), which is also the lowest band where lenders extend their best rates without further qualification.

One trap catches nearly everyone who checks a free score. The number on Credit Karma or a banking app is usually a VantageScore, not a FICO, and VantageScore draws its band lines in different places: its "good" tier runs 661 to 780, wider than FICO's 670 to 739. A 745 is "very good" on FICO but merely "good" on VantageScore; a 665 is "good" on VantageScore but only "fair" on FICO. Same underlying credit file, different label. That is why your monitoring app and your mortgage lender can quote you numbers 20 or 30 points apart.

CIBIL score ranges in India

TransUnion CIBIL operates on a 300 to 900 scale, and Indian lenders treat 750 and above as the benchmark for a good score. The commonly quoted bands:

| CIBIL band | Range | What it unlocks in India |

|---|---|---|

| Poor | 300-649 | Most unsecured credit declined; secured loans at high rates |

| Average | 650-699 | Some cards and personal loans at premium rates, sometimes with a co-applicant |

| Good | 700-749 | Most products at standard published rates |

| Excellent / lender-preferred | 750-900 | Best home loan, car loan, and credit card rates |

Marketing blogs draw these cutoffs in slightly different places, which is where the confusion comes from. The most authoritative segmentation is CIBIL's own risk-tier structure, published in its March 2024 newsroom data: subprime 300 to 680, near prime 681 to 730, prime 731 to 770, prime plus 771 to 790, and super prime 791 to 900. Notice that the bureau itself starts treating you as "prime" at 731, a little below the popular 750 line.

India has four RBI-licensed bureaus. CIBIL, Experian, Equifax, and CRIF High Mark all score on the same 300 to 900 range, though their exact cutoffs vary. Banks usually pull CIBIL first and check a second bureau for large loans, which means, as in the US, you effectively have several scores across bureaus with no single official one.

What is the highest credit score?

The highest possible FICO score is 850 and the highest possible CIBIL score is 900. This single difference drives a huge amount of search traffic and just as much confusion, because a reader who has only ever seen one system assumes the other shares its ceiling. It does not: a "perfect" US score is 850, and a "perfect" Indian score is 900.

Both are genuinely rare, and reaching them buys almost nothing. Only 1.76% of US consumers held a perfect FICO 850 as of March 2025, the highest share since 2009 (Experian); under the newer VantageScore 4.0 model, just 0.24% of adults hit 850, roughly two in a thousand. In India, lenders describe a perfect 900 as near-impossible for an ordinary borrower and, more to the point, say they treat 850 and 900 identically. The practical ceiling for pricing is around 750 to 760 in both countries. Above it, the rate you are quoted stops improving even as the number keeps climbing.

The people who do reach the top share one habit worth borrowing without chasing the score itself: 850-holders use only about 4% of their available credit, against a US average near 28%. Low utilisation, not a magic number, is what the top tier has in common.

What a good score actually saves you

The clearest way to see why the band matters is on a long loan, where a small rate gap compounds for decades. These are illustrative spreads; for today's exact rates, check the live sources listed at the end.

Take a Rs 50 lakh Indian home loan over 20 years:

| CIBIL band | Typical home loan rate | EMI on Rs 50 lakh | Total interest |

|---|---|---|---|

| 800+ | 8.50% | Rs 43,400 | Rs 54.2 lakh |

| 750-799 | 8.75% | Rs 44,200 | Rs 56.1 lakh |

| 700-749 | 9.25% | Rs 45,800 | Rs 59.9 lakh |

| 650-699 | 10.00% | Rs 48,300 | Rs 65.9 lakh |

| Below 650 | 11%+ or declined | Rs 51,600+ | Rs 73.8 lakh+ |

The 800-plus borrower pays roughly Rs 19.6 lakh less in total interest than the sub-650 borrower on the exact same Rs 50 lakh loan. For Indian credit cards the score changes approval odds and credit-limit size more than the headline APR, which clusters in the 36 to 42% effective range across issuers regardless of score. On personal and auto loans the published-rate spread between excellent and poor CIBIL borrowers is typically 4 to 10 percentage points.

The US pattern is the same on a $300,000 30-year fixed mortgage:

| FICO band | Approximate rate | Monthly payment | Total interest over 30 years |

|---|---|---|---|

| 760+ | 6.50% | $1,896 | $382,400 |

| 700-759 | 6.85% | $1,966 | $407,800 |

| 660-699 | 7.20% | $2,036 | $433,000 |

| 620-659 | 7.65% | $2,127 | $465,500 |

| Below 620 | 8.50%+ | $2,307 | $530,500+ |

The 760-plus borrower pays about $148,000 less in total interest over 30 years than the sub-620 borrower on the identical loan. On US credit cards, the Federal Reserve G.19 report put the average APR on accounts assessed interest near 24%; borrowers at FICO 740-plus tend to see 18 to 22%, while those under 620 see 28 to 32% when approved at all.

Read both tables together and the same conclusion falls out: a good score is not a grade, it is a price. The steepest savings per point come from moving out of the fair band into the lender-preferred band, roughly 660 to 760 on FICO. For the specific factors that move the number, see which factors actually affect your score.

What is the average credit score?

The average US FICO score was 713 in 2025, down two points from 715 in 2024 (Experian). That average hides a steady climb with age, because older borrowers have longer credit histories and lower balances:

| Generation | Average FICO (2025) |

|---|---|

| Gen Z (18 to 28) | 678 |

| Millennials (29 to 44) | 689 |

| Gen X (45 to 60) | 709 |

| Boomers (61 to 79) | 747 |

| Silent (80+) | 760 |

Only the two oldest groups sit above the 740 best-rate line on average, which tells younger borrowers something reassuring: a below-average score at 25 is normal and mostly a function of time.

India does not publish a single official average CIBIL score, and any specific national number floating around lender blogs should be treated with caution. The defensible framing is that lenders describe the 650 to 699 range as the average band, and a 750-plus score puts a borrower in roughly the top 14% of the credit-active population. Credit awareness is rising fast: about 119 million Indians had checked their CIBIL score by March 2024, up 51% year on year, and more than three-quarters of them were Gen Z or Millennials.

How to check your credit score

Both countries give you free, no-cost ways to see your score, and checking it yourself never lowers it.

In India, the RBI requires all four bureaus (CIBIL, Experian, Equifax, CRIF High Mark) to provide one free full credit report per year per person. Fintech platforms such as Paisabazaar, BankBazaar, and Cred also show a free CIBIL score, and many banks display it inside their app.

In the US, annualcreditreport.com is the federally mandated free source for Experian, Equifax, and TransUnion reports, though those reports show your history without a score attached. For free FICO scores, several card issuers (Discover, Citi, Capital One, Bank of America) print one on the monthly statement.

Checking your own score is a soft inquiry with no effect. Only a hard inquiry, when a lender pulls your file to process an application, moves the number, and only slightly. Monitoring your score monthly is normal and harmless.

Common misconceptions about a good score

The first misconception is that 850 or 900 is the target. It is not. The best rates arrive at 740 (FICO) or 750 (CIBIL), and the top few dozen points are cosmetic for pricing, as the rarity numbers above show.

The second is that a good score is permanent once earned. A score is a snapshot of your file this month, so it moves as balances, new applications, and account ages change. A good score is maintained, not banked.

The third is that there is one universal credit score. A US borrower has at least three FICO 8 scores (one per bureau), plus FICO 9 and 10, several industry-specific FICO variants, and a VantageScore; an Indian borrower has a score at each of four bureaus. They can differ by 10 to 40 points, and the lender approving a specific loan is the only one who knows which model they used.

What deliberately sits outside this post: the mechanics of how the number is built (payment history, credit age, credit mix) live in how credit scores are calculated, the single biggest lever gets its own guide in how utilization affects your score, and the underlying file every score is computed from is covered in what a credit report shows. This piece stays on what the resulting number counts as.

Frequently asked questions

What is a good credit score? A good credit score is 670 or above on FICO (which runs 300 to 850) and 750 or above on CIBIL (which runs 300 to 900). On FICO, 670 to 739 is "good", 740 to 799 is "very good", and 800 to 850 is "exceptional". In India, 700 to 749 is treated as good and 750-plus is the lender-preferred band where the best rates open up. The average US FICO score was 713 in 2025 (Experian).

What is the highest credit score? The highest FICO score is 850 and the highest CIBIL score is 900. Both are rare: only 1.76% of US consumers held a perfect 850 as of March 2025 (Experian), and a perfect 900 CIBIL is described by lenders as near-impossible. It also does not matter much, because lenders treat scores from roughly 750 upward almost identically, so there is little practical gain above that level.

Is a 700 credit score good? Yes. 700 sits in the "good" band on FICO (670 to 739) and in the good band on CIBIL (700 to 749). It qualifies you for most mainstream credit at reasonable rates, but not the best-advertised rates, which generally need 740-plus on FICO or 750-plus on CIBIL. 700 is also slightly below the 713 US average, so there is clear room to improve.

Is 750 a good CIBIL score? Yes. 750 is the widely-used "good" or "ideal" CIBIL threshold in India: it is the level most banks, NBFCs, and fintech lenders prefer for the fastest approvals, lower interest rates, and higher limits. A 750-plus borrower can typically access larger unsecured loans (roughly Rs 2 lakh to Rs 25 lakh, or up to 8 to 10 times monthly income) and premium credit cards.

What is the average credit score? In the US the average FICO score was 713 in 2025, down slightly from 715 in 2024 (Experian). It climbs with age: about 678 for Gen Z, 689 for Millennials, 709 for Gen X, 747 for Boomers, and 760 for the Silent Generation. In India there is no single official published average, but lender data puts the typical band around 650 to 699.

The bottom line

A good credit score is 670 or higher on FICO and 750 or higher on CIBIL, the levels where lenders quote their best published rates. The maximums differ (850 in the US, 900 in India), but both are rare and neither is worth chasing, because pricing stops improving around 750 to 760 in both systems.

The reason to care is money, not the number itself. Move from the fair band into the lender-preferred band and, on a 20 to 30 year home loan, you save roughly Rs 19 lakh in India or close to $148,000 in the US in total interest. Most people already sit one band below that line, which means the score is a price, and it is usually a price you can lower.

Sources

- myFICO, What Is a Good Credit Score, myfico.com/credit-education/credit-scores

- Experian, What Is the Average Credit Score in the U.S.? (713 in 2025, band distribution, average by age), experian.com/blogs/ask-experian/what-is-the-average-credit-score-in-the-u-s

- TransUnion CIBIL Newsroom, 100 million Indians monitored their CIBIL score (official risk tiers, 119M consumers), newsroom.transunioncibil.com

- Freddie Mac, Primary Mortgage Market Survey, freddiemac.com/pmms

- Federal Reserve, Consumer Credit G.19, federalreserve.gov/releases/g19/current

- Reserve Bank of India, Database on Indian Economy (bank lending rates), rbi.org.in

You might also like

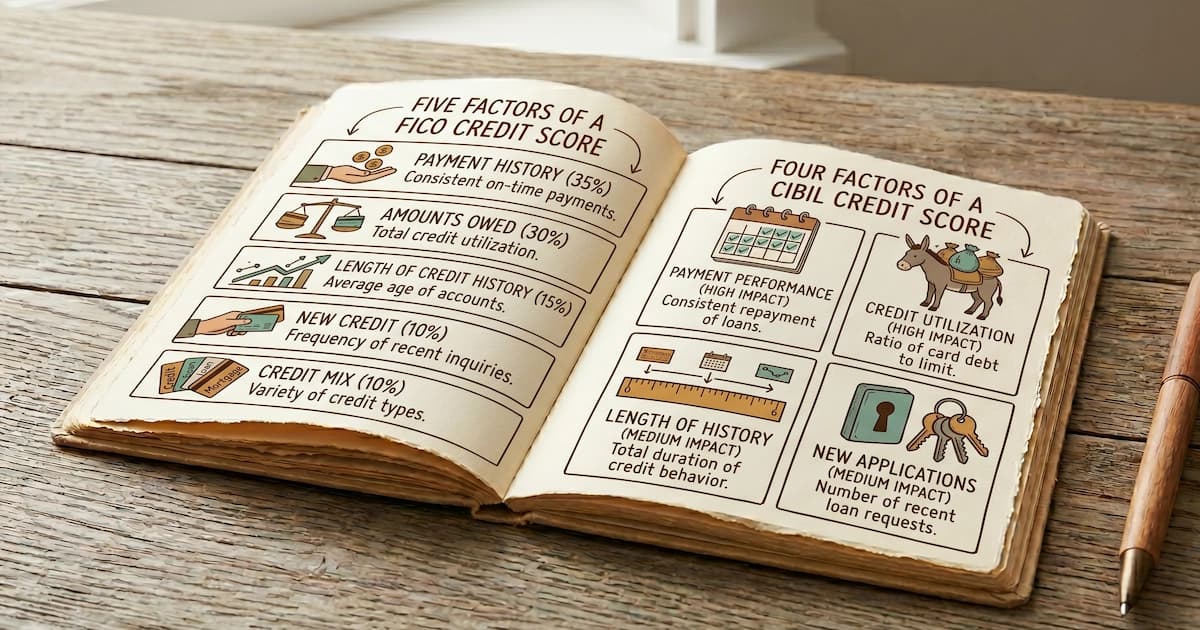

How credit scores are calculated by FICO in the US (5 factors) and TransUnion CIBIL in India (4 factors), with the exact weights and what each one measures.

9 min read

What is a credit report? A plain-English explanation of what's on it, where it comes from, who can see it, and how it differs from a credit score.

8 min read

A good credit utilization ratio is under 30%, and top scores sit under 10%. Why 30% is not an official FICO or CIBIL rule, and how to lower yours fast.

13 min read